This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The S&P 500 currently trades at a price to book value of 4.2, suggesting that book value accounts for less than 20% of the S&P 500’s market value. The remaining 80%, appears nowhere in these firms’ balance sheets—it is invisible to contemporary accounting techniques and constitutes “dark accounting matter.”

Consequently, you can only value the equity in a bank, and by extension, the only pricing multiples you can use to price banks are equity multiples (PE, Price to Book etc.).

Following that rule book, I looked at the effects of inflation on the levers that determines value, in the graph below: Put simply, the effects of inflation on firm value boil down to the impact inflation has on expected cash flows/growth and risk.

With the Japanese economy sluggish, Wu points out, the TSE has become concerned about the low price-to-book ratios of its listed companies, including banks; half of Prime members traded below book last year. Now they’re thinking more strategically about how to allocate capital.”

Searching for stocks with low price-to-book ratios was a good indication of a potential bargain. This makes the task of valuation much more difficult, but also a lot more interesting. In the past, market valuations often mirrored the reported balance sheet.

Valuation Price-to-book (P/B) is one of the multiples used for valuing insurance stocks. The consensus mark for 2025 earnings is pegged at $9.83 per share, suggesting an improvement of 13.4% from the 2024 estimate. The same for revenues is $76.5 billion, hinting at a 4.6% increase from the 2024 estimate.

I also looked at how inflation plays out on equity sub-groupings, on two dimensions, the first being market capitalization and the second being price to book, with the former becoming a stand-in for the vaunted small cap premium and the latter for the value versus growth question.

By comparing key financial metrics such as price-to-earnings (P/E) ratios, price-to-sales (P/S) ratios, and price-to-book (P/B) ratios, analysts can estimate the target company’s value. In the context of M&A, asset-based valuation techniques such as book value and liquidation value are commonly employed.

Different Methods of Benchmark Valuation There are several ways to conduct a benchmark valuation, each with its unique focus and methodology: Price-to-Earnings Ratio (P/E) The P/E ratio compares a company’s current share price to its earnings per share (EPS). It’s one of the most popular metrics for evaluating stock performance.

Asset-based methods like Adjusted Book Value, Liquidation Value, and Replacement Cost consider the worth of tangible assets. Excerpted from the book “Valuation for Mergers and Acquisitions” by Barbara S. Income-based methods such as Discounted Cash Flow analysis focus on future cash flows to determine value. Petitt and Kenneth R.

Metrics such as price-to-earnings (P/E) ratios, price-to-book (P/B) ratios, and other multiples are used to evaluate how the security compares to its peers. Comparative Analysis : Also known as relative valuation, this approach involves comparing the security to similar assets in the market.

By analyzing factors like the price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, and enterprise value-to-EBITDA (EV/EBITDA) ratio, companies can determine if their shares are undervalued or overvalued compared to peers.

By analysing factors such as the price-to-earnings (P/E) ratio, the price-to-book (P/B) ratio, and the enterprise value-to-EBITDA (EV/EBITDA) ratio, companies can determine whether their shares are undervalued or overvalued relative to its peers.

By analyzing the valuation multiples (such as price-to-sales or price-to-book ratios) of comparable businesses, you can estimate a valuation range for the company in question. This method relies on finding appropriate comparables.

Metrics such as price-to-earnings (P/E) ratios, price-to-book (P/B) ratios, and other multiples are used to evaluate how the security compares to its peers. Comparative Analysis : Also known as relative valuation, this approach involves comparing the security to similar assets in the market.

Metrics such as price-to-earnings (P/E) ratios, price-to-book (P/B) ratios, and other multiples are used to evaluate how the security compares to its peers. Comparative Analysis : Also known as relative valuation, this approach involves comparing the security to similar assets in the market.

Slicing the data based on sector yields the following: Against, there are no surprises, with energy being the only sector to post positive returns and with consumer discretionary and technology generating the most negative returns.

Book value is the value attributable to shareholders in case the company sells all its assets and repays its liabilities (also called liquidation value). A price-to-book ratio of less than 1x indicates that the market values the net assets less than the balance sheet suggests. Fundamentals, Valuation, Momentum, and Risk (FVMR).

The valuation is based on key financial metrics such as Price-to-Earnings (P/E) ratios, Price-to-Sales (P/S) ratios, or Price-to-Book (P/B) ratios. Comparable Company Analysis (CCA): CCA involves comparing the target company to similar publicly traded companies.

Interest Rates and Value As interest rates have risen, the discussion in markets has turned ito the effects that these rates will have on stock prices.

For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive. Standard deviation in stock price 2. Price to Book 3. High-Low Price Risk Measure 5. EV/Sales and Price/Sales 5. Cost of Equity 1.

Key Financial Ratios: Ratios such as Price-Earnings Ratio (P/E), Price-to-Book Ratio (P/B), and Debt-to-Equity Ratio provide valuable insights into the company's performance and market position. Understanding the company's financial health is fundamental to valuation.

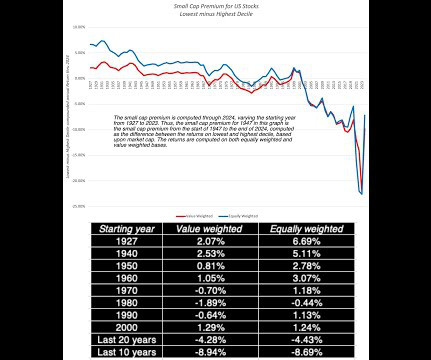

There is a risk of reading too much into the data in this table, but the three best decades for low price to book stocks were 1940-49, 1970-79 and 1980-89, the three decades when inflation was high, and in two of those decades, inflation was much higher than expected.

Consider, for instance, an investor who picks stocks based upon price to book ratios, who finds a stock trading at a price to book ratio of 1.5. buy stocks that trade at less than book value or trade at PEG ratios less than one) for individual stocks.

One key emphasis is on the Price to Book Value multiple. The Price to Book Value multiple, which compares a bank's market value to its book value, becomes crucial. Emphasizing Unique Considerations: Valuing a bank requires a distinct approach due to the nature of its operations.

MVA can be understood as the Price-to-Book ratio; however, the book value has been refined to account for economic adjustments. The Market Value Added (MVA) Spread from the ISS EVA framework serves to assess company valuation.

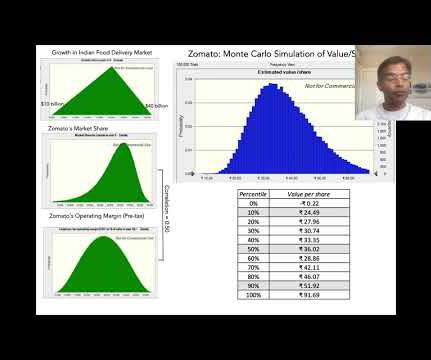

The second is the cost of capital, a number that most valuation classes and books (including mine) belabor to the point of diminishing returns. Finally, dismissing Zomato as an investment, just because it does not make money now, or fails to meet some conventional value tests on pricing (PE, Price to Book), is investing malpractice.

In the next section, I look at stock returns for companies in different price to book deciles, in a simplistic assessment of the value premium. As with the size premium, low price to book (value) stocks have struggled to deliver in the twenty first century, and as with the small size premium, investors have waited for it to return.

You see similar movements in the price to book, where the stock has gone from trading under book value to 6.7 times book value, and the enterprise value, which was less than revenue in 2016-21 to 2.71 times revenues in the most recent two years.

With these characteristics, the accounting balance sheets for these companies will be identical right after they start up, and the book value of equity will be $60 million in each company. The first is that if markets are efficient, the price to book ratios will reflect the quality of these companies.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content