This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

An investor who buys a good bank at too high a price, given its goodness, will underperform one who buys a bad bank at too low a price, given its badness. Consequently, you can only value the equity in a bank, and by extension, the only pricing multiples you can use to price banks are equity multiples (PE, Price to Book etc.).

At the start of the year, the consensus of market experts was that this would be a difficult year for markets, given the macro worries about inflation and an impending recession, and adding in the fear of the Fed raising rates to this mix made bullishness a rare commodity on Wall Street. That pessimism was not restricted to market outlooks.

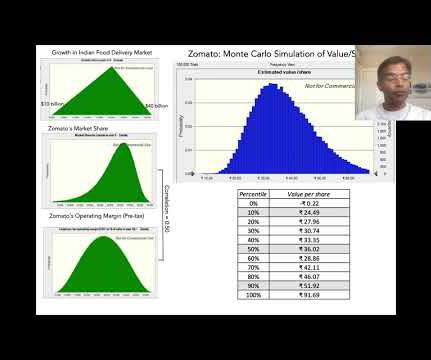

Zomato, an Indian online food-delivery company, was opened up to public market investors on July 14, 2021, and its market debut is being watched for clues by a number of other online ventures in India, waiting in the wings to go public. The Zomato IPO clocks in at 420 pages , much of it designed to bore readers into submission.

In my last post, I talked about the ritual that I go through every year ahead of my teaching each spring, and in this one, I will start on the first of a series of posts that I make at the start of each year, where I look at data, both macro and company-level. That is not true!

Market-based methods like Comparable Companies Analysis and Precedent Transactions Analysis offer relative measures of value based on market data. Income-based methods such as Discounted Cash Flow analysis focus on future cash flows to determine value.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

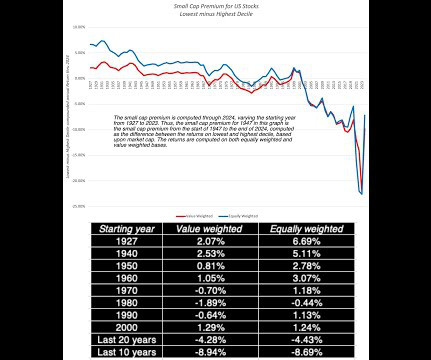

I follow up by looking at companies broken down by market capitalization, with an eye on whether the much-vaunted small cap premium has made a comeback. In the next section, I look at stock returns for companies in different price to book deciles, in a simplistic assessment of the value premium. in the last 20 years.

The Lead In As noted in the introductory paragraph, I start from a position of ignorance about the Adani Group, and it thus made sense to fill in that gap. First, they are infrastructure businesses , requiring large up-front investments and having long gestation periods, with regulatory and government oversight.

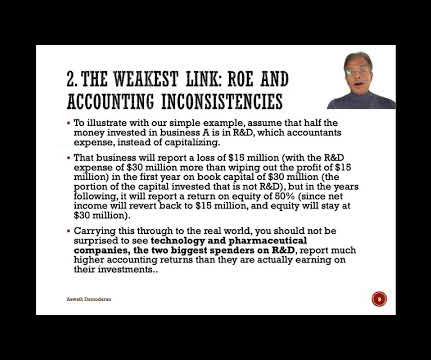

I pointed to the flaw in the logic, but the comments thereafter suggested such deep confusion about what returns on equity or capital measure, and what comprises an efficient market, that I think it does make sense to go back to basics and see if some of the confusion can be cleared up.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content