This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

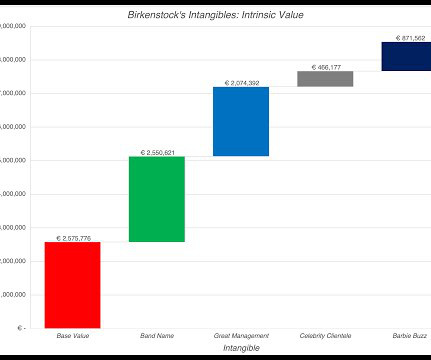

The Value of Intangible Assets Accounting has historically done a poor job dealing with intangible assets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. trillion below their values from the start of 2022. that was lost last year.

Real estate and utilities are the two sectors that have not come back fully from the COVID effect, but materials, technology and communication services are now reporting significantly higher earnings that before the shut down.

This is accomplished through methods like Comparable Company Analysis, Precedent Transaction Analysis, and MarketCapitalization, which collectively offer insights into the company’s value within the context of the broader market landscape. It represents the total marketvalue of the company’s equity.

Asset-Based Approaches: Asset-based approaches determine a company’s value based on its net asset value (NAV). Two commonly used asset-based approaches are: a) BookValue Method: The bookvalue method calculates a company’s net asset value by subtracting total liabilities from the fair marketvalue of total assets.

Asset-Based Approaches: Asset-based approaches determine a company’s value based on its net asset value (NAV). Two commonly used asset-based approaches are: a) BookValue Method: The bookvalue method calculates a company’s net asset value by subtracting total liabilities from the fair marketvalue of total assets.

million in estimated cost saving synergies), this acquisition positions SMGI as a leading regional transportation and logistics player across multiple markets in the United States. With the completion of this transaction, SMGI's balance sheet is significantly improved, including a large increase in the bookvalue of the combined company.

That, for instance, is the only way to explain why older telecom companies, which developed a practice of borrowing large amounts during their time as monopoly phone businesses, continue that practice, even as their business have evolved into intensely competitive, technology businesses. at least with technology companies).

Thus, an analyst who follows young technology companies may decide that paying ten times revenues for a company is a bargain, if all of the companies that he tracks trade at multiples greater than ten times revenues. buy stocks that trade at less than bookvalue or trade at PEG ratios less than one) for individual stocks.

For example, I have seen it asserted that a stock that trades at less than bookvalue is cheap or that a stock that trades at more than twenty times EBITDA is expensive. Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like marketcapitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

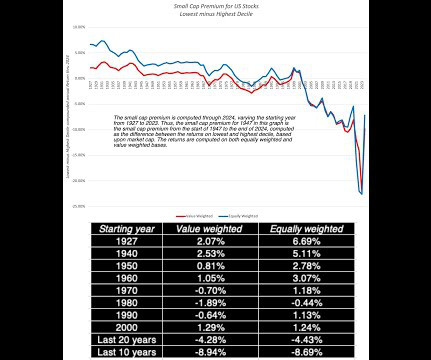

I follow up by looking at companies broken down by marketcapitalization, with an eye on whether the much-vaunted small cap premium has made a comeback. In the process, I also look how much the market owes its winnings to its biggest companies, with the Mag Seven coming under the microscope. trillion) in market cap.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content