This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

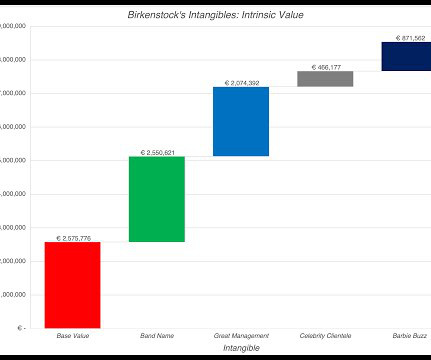

The Value of Intangible Assets Accounting has historically done a poor job dealing with intangible assets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent.

This is accomplished through methods like Comparable Company Analysis, Precedent Transaction Analysis, and Market Capitalization, which collectively offer insights into the company’s value within the context of the broader market landscape. It represents the total market value of the company’s equity.

Real estate and utilities are the two sectors that have not come back fully from the COVID effect, but materials, technology and communication services are now reporting significantly higher earnings that before the shut down.

In the DCF method, the value of the business is calculated by estimating the future cash flows of the business, with a discount rate applied. In the CCA method, valuation multiples such as P/E ratio, EV/Revenue ratio, and EV/EBITDA ratio, provide benchmarks for estimating value by comparing financial metrics to publicly traded companies.

In the DCF method, the value of the business is calculated by estimating the future cash flows of the business, with a discount rate applied. In the CCA method, valuation multiples such as P/E ratio, EV/Revenue ratio, and EV/EBITDA ratio, provide benchmarks for estimating value by comparing financial metrics to publicly traded companies.

Asset-based methods like Adjusted BookValue, Liquidation Value, and Replacement Cost consider the worth of tangible assets. These ratios, like the EBITDA multiple, compare a company’s financial performance (EBITDA, revenue, etc.) to its market value.

In general, correcting the accounting mistake will increase operating and net profits, at most firms, as well as book equity and invested capital, and for most firms that spend money on R&D, capitalizing R&D will lower accounting returns (return on equity and return on invested capital). billion to $49.3 billion , as reported.

Candidates should highlight their commitment to staying updated on industry trends, regulations, and emerging technologies. On the other hand, Equity Value solely concentrates on the shareholders' stake in the company. Financial Criteria: Dive deeper into revenue, EBITDA, and other financial metrics for more specific comparisons.

Cleaning Business Valuation Methods Business appraisers typically use three primary approaches when valuing a cleaning business: Market Approach The market approach compares a cleaning service business to similar businesses recently sold in the open market. They may use revenue, EBITDA, or SDE multiples. Schedule a Free Consultation!

The successful closing of this strategic acquisition not only approximately doubles SMGI's annual revenue and increase its adjusted EBITDA, but also brings operational and revenue diversification, strengthens the Company's balance sheet and adds exceptional expertise to its leadership team. million (including $2.5

One is to compute the taxes you would have paid on operating income, if it had been fully taxable, to get after-tax operating income and margin , and the other is to add back depreciation to operating income to get EBITDA and EBITDA margin.

That is, were the companies in those transactions valued as a multiple of EBIT , EBITDA , revenue, or some other parameter? If you figure out what the key valuation parameter is, you can examine at what multiples of those parameters the comparable companies were valued. How to Value an Advertising Business.

Among the sectors, energy stands out, generating the highest margins globally, and the second highest, after technology firms in the United States. In maturity, with debt entering the financing mix, net margins become good measures of profitability, and in decline, as earnings decline and capital expenditures ease, EBITDA margins dominate.

Cash generating capacity : Debt payments are serviced with operating cash flows, and the more operating cash flows that firms generate, as a percent of their market value, the more that they can afford to borrow. Debt to EBITDA, Interest Coverage Ratios If debt to capital is not a good measure for judging over or under leverage, what is?

That is still true for the average company in the industry: it is more defensive than something like technology or financial institutions. Overall, though, there are fewer industry-focused independent/boutique firms than in sectors like technology or healthcare.

By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time. For example, I have seen it asserted that a stock that trades at less than bookvalue is cheap or that a stock that trades at more than twenty times EBITDA is expensive.

The PE ratio for the stock has gone from a modest 15 times earnings in the 2016-21 time period to 214 times earnings in the most recent two years, and the enterprise value has jumped from about 12 times EBITDA during 2016-21 to 53 times EBITDA in the most recent two years. times revenues in the most recent two years.

Breaking down companies by (S&P) sector, again both in numbers and market cap, here is what I get: While industrials the most listed stocks, technology accounts for 21% of the market cap of all listed stocks, globally, making it the most valuable sector. Standard Deviation in Equity/Firm Value 2. BookValue Multiples 3.

Breaking down the remaining sectors, real estate and utilities are the heaviest users of debt, and technology and health care the lightest. Across regions, and looking just at non-financial firms, the US has the highest debt ratio, in bookvalue terms, but among the lowest in market value terms.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content