This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

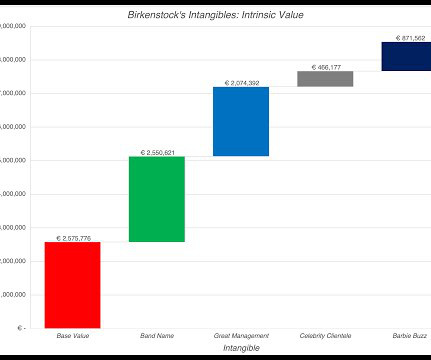

In this post, I will look at another initial public offering, Birkenstock, that is likely to get more attention in the next few weeks, given that it is targeting to go public at a pricing of about €8 billion, for its equity, in a few weeks. So, how far has accounting come in bringing intangible assets on to balance sheets?

Ask anyone interested in distressed debt hedge funds for “the pitch,” and they’ll probably mention one of the following: “It’s like long/short equity or credit , but more interesting!” Distressed investing offers equity-like returns with lower risk.” Distressed assets offer non-correlated returns, similar to global macro.”

After paying taxes on this income, the residual amount represents net income, the final measure of equity earnings, and the basis for computing earnings per share and other widely used measures of profitability used by equity investors.

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. The ratio is then used in a simple multiplication calculation, to determine the value of the company in question. Broadly, there are two different common ways to value using multiples. .

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. The ratio is then used in a simple multiplication calculation, to determine the value of the company in question. Broadly, there are two different common ways to value using multiples. .

Adjusted Net BookValue Adjusted Net BookValue is the BookValue of a business that has been adjusted to reflect the current market value of the assets and liabilities of a company. In this case, an adjustment to the value of these assets is required to determine Adjusted Net BookValue.

Market-Based Business Valuation Formula For a market-based calculation, use: CV = (EBITDA x 1.5) – (Current Liabilities x 0.5) Or V = (EBITDA * 1.3) / (Revenue – COGS) As an example, if a business's EBITDA is $300,000 and current liabilities are $50,000, the calculation would be: ($300,000 x 1.5) - ($50,000 x 0.5) = $425,000.

The second is to look at the industry group or sector that a company is in, and then follow up by classifying that industry group or sector into high or low growth; for the last four decades, in US equity markets, tech has been viewed as growth and utilities as mature.

This is accomplished through methods like Comparable Company Analysis, Precedent Transaction Analysis, and Market Capitalization, which collectively offer insights into the company’s value within the context of the broader market landscape. It represents the total market value of the company’s equity.

That is especially true when the buyer is a private equity group or other type of “financial” buyer, which is the case in seven out of 10 deals that we have closed over the last several years. Strengthen your ratios: working capital, debt-to-equity, “quick,” price-to-earnings, return on equity, etc.

Market-based methods like Comparable Companies Analysis and Precedent Transactions Analysis offer relative measures of value based on market data. Income-based methods such as Discounted Cash Flow analysis focus on future cash flows to determine value. to its market value.

Understanding the Concept: In essence, FCFF encapsulates the cash that can be distributed to both debt and equity holders after meeting operational needs and capital expenditures. The resulting value represents the cash available to all contributors of capital—both debt and equity. What is Free Cash Flow to Equity?

In the DCF method, the value of the business is calculated by estimating the future cash flows of the business, with a discount rate applied. In the CCA method, valuation multiples such as P/E ratio, EV/Revenue ratio, and EV/EBITDA ratio, provide benchmarks for estimating value by comparing financial metrics to publicly traded companies.

In the DCF method, the value of the business is calculated by estimating the future cash flows of the business, with a discount rate applied. In the CCA method, valuation multiples such as P/E ratio, EV/Revenue ratio, and EV/EBITDA ratio, provide benchmarks for estimating value by comparing financial metrics to publicly traded companies.

It is in pursuit of answering these questions that accountants generate financial statements, and the three most basic are: The balance sheet , which summarizes what a firm owns and owes at a point in time, as well as an estimate of what equity is worth (through accounting eyes).

Discount Future Cash Flows – either by using the Mid-Year discount or a simple discount period, it is fairly simple to calculate the present value of future cash flows. This action will cause fluctuations in the overall value of equity and debt ratio. Issues faced when using a relative valuation method. Conclusion.

One is to compute the taxes you would have paid on operating income, if it had been fully taxable, to get after-tax operating income and margin , and the other is to add back depreciation to operating income to get EBITDA and EBITDA margin.

Because a strategic purchase may be based on factors other than multiples of earnings or EBITDA, a strategic buyer might be willing to pay more for your business than would a financial buyer, despite the latter’s presumably deeper pockets. Selling to a Private Equity Group. Preparation.

The successful closing of this strategic acquisition not only approximately doubles SMGI's annual revenue and increase its adjusted EBITDA, but also brings operational and revenue diversification, strengthens the Company's balance sheet and adds exceptional expertise to its leadership team. million (including $2.5

To fund the business, you can either use borrowed money (debt) or owner's funds (equity), and while both are sources of capital, they represent different claims on the business. Even government-owned businesses fall under its umbrella, with the key difference being that equity is provided by the taxpayers.

Power and Utilities Investment Banking Definition: In power/utilities IB, bankers advise companies that produce, transmit, and distribute electricity, natural gas, and water on raising debt and equity and completing mergers and acquisitions. For example, let’s say the company’s Rate Base is $1,000, as in the Lazard example above.

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Free Cash Flows to Equity (Potential Dividends) The most intuitive way to think about potential dividends is to think of it as the cash flow left over after every conceivable business need has been met (taxes, reinvestments, debt payments etc.).

By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time. For example, I have seen it asserted that a stock that trades at less than bookvalue is cheap or that a stock that trades at more than twenty times EBITDA is expensive.

Return on Equity 1. Equity Risk Premiums 2. Costs of equity & capital 4. Costs of equity & capital 1. Fundamental Growth in Equity Earnings 2. Return on Equity 2. Standard Deviation in Equity/Firm Value 2. BookValue Multiples 3. EBIT & EBITDA multiple s 5.

Adani's Debt Load The investment side of the Adani story is not complete without bringing in the financing part, since the money for these investments has to come from somewhere, either internally, residual cash flows from existing operations, or externally, from new debt or equity.

Thus, as you peruse my historical data on implied equity risk premiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

The Debt Trade off As a prelude to examining the debt and equity tradeoff, it is best to first nail down what distinguishes the two sources of capital. To me, the key distinction between debt and equity lies in the nature of the claims that its holders have on cash flows from the business.

The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market. The first is the price earnings ratio , partly because in spite of all of its faults, it remains the most widely used pricing metric in the world.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content