This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. At the start of 2022, the ten sectors (US) with the highest and lowest relative risk (unlettered betas), are shown below.

The various problems facing the company led the court to embrace the respondents’ theory that SWS would continue to face an uphill climb given its relatively small size, which prevented it from scaling its substantial regulatory, technological, and back-office costs. With regard to beta, the court found fault with both side’s approach.

Changes in tax regulations, technology advancements, and shifts in customer preferences can impact the future prospects and growth potential of the business. Technology and Infrastructure In today's digital age, the technology and infrastructure employed by a tax preparation business can greatly influence its value.

Equipment, Technology, and Infrastructure The quality and condition of equipment, technology, and infrastructure directly influence the value of a disaster restoration business. Stay updated on the latest advancements, changes in regulations, and emerging technologies that can impact the business's value.

Kevin holds an MBA in finance from Georgia State University and a Bachelors in Chemical Engineering from the Georgia Institute of Technology. He is member of the Beta Gamma Sigma Honor Society, Financial Executives International, and the National Association of Corporate Directors (NACD).

Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Cost of Equity 1.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. at least with technology companies). Me-to-ism : The second and almost as powerful a force in determining debt policy is peer group behavior.

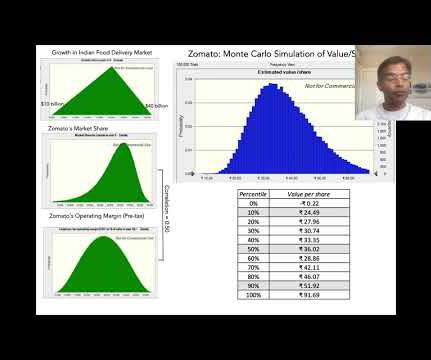

It would be churlish on my part to take issue with the bloat and selective disclosure in Zomato's prospectus, since they are following the script that other technology companies around the world have written for going public, but it is frustrating to read through 420 pages, and still be left in the dark on key numbers.

In short, if you don't like betas and have disdain for modern portfolio theory, your choice should not be to abandon risk measurement all together, but to come up with an alternative risk measure that is more in sync with your view of the world.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content