This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the world of finance and investing, the concept of beta plays a vital role in assessing an investment’s risk and volatility. Whether you’re a seasoned investor or new to the market, understanding beta can empower you to make informed decisions. What is beta and how do you calculate beta?

It helps an investor understand what to expect to earn in relation to the risk-freerate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-freerate by buying the risk-free asset. beta of a stock). E(r) = Rf + ??(Rm

What is Beta in Finance, and why is it essential for a business valuation? Are you considering evaluating a business using an excel template without understanding Beta in Finance? In statistics, beta is defined as the slope of a straight line. The beta measures the return of the stock relative to the market return.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

Risk-freerate . The expected return of the market . The systematic risk of the security (Beta). The market value of the stock . The growth rate of dividends . Where R(e) = expected return on investment, Rf = risk-freerate, Rm = expected return of the market, and ??

The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate. Different types of discount rates such as risk-freerate, cost of equity, or cost of debt, are used contextually in financial analysis.

The expected return on an asset is determined by the risk-freerate of return with the addition of the asset’s beta to each macroeconomic factor that impacts the return on the asset multiplied by the risk premium of those factors. Inflation rate: ß = 0.6, The risk-freerate is 5%.

Convertible Arbitrage Definition: Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; the fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall marketrisk.

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM). A beta of 1.0

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM). A beta of 1.0

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM). A beta of 1.0

The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The marketrisk premium is calculated from a marketrate of return less a risk-freerate. Suitability and limitation. Conclusion.

You usually link Revenue to market share * market size or units sold * average selling price, with expenses linked to Capacity, unit sales, or another top-level driver. DTM’s Levered Beta at this time was only 0.80, but I increased it to 1.00

The important figure there is r, which we’re using as the discount rate in this whole equation. But here, we use what interest we could get from an alternative investment in the market, called the MarketRate. This is the rate of return you’d get if you invested your money today instead. . Rf = Risk-freeRate.

Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments. That tells me three things.

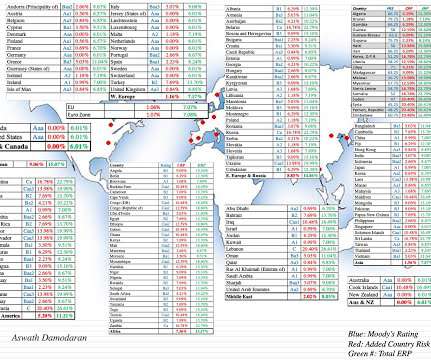

I know that there are some of you, who distrust ratings agencies, arguing that they have regional and other biases and/or that they do not adjust ratings in a timely fashion. Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity risk premium, and equity risk premiums will vary across countries.

Capital Constrained Clearing Rate : The notion that any investment that earns more than what other investments of equivalent risk are delivering is a good one, but it is built on the presumption that businesses have the capital to take all good investments. More on that issue in a future data update post.)

In my last three posts, I looked at the macro (equity risk premiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

Thus, looking at only the companies in the S&P 500 may give you more reliable data, with fewer missing observations, but your results will reflect what large market cap companies in any sector or industry do, rather than what is typical for that industry.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content