This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on marketcapitalization and price to book ratios.

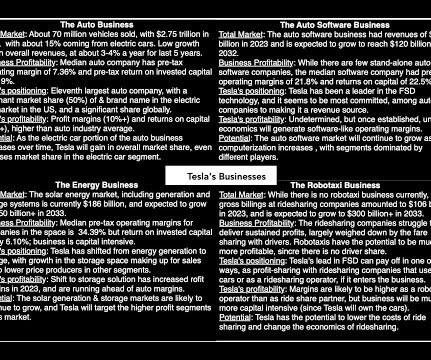

I was planning to start this post by telling you that Tesla was back in the news, but that would be misleading, since Tesla never leaves the news. I profited mightily on that investment, but I sold too soon , when Tesla's marketcapitalization hit $150 billion, and just before COVID put the company on a new price orbit.

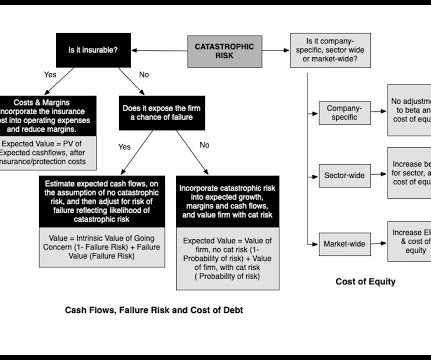

If you start enumerating every risk a business is exposed to, you will find yourself being overwhelmed by that list, and it is for that reason that I categorize risk into the groupings that I described in an earlier post on risk.

That may reflect the concern that once a person or entity starts borrowing to fund its needs, it is easy to overuse debt, and risk its wellbeing in the process. In that case, the optimal debt ratio for a company is the one that maximizes value, not necessarily the one at which the cost of capital is minimized.

In my last post, I talked about the ritual that I go through every year ahead of my teaching each spring, and in this one, I will start on the first of a series of posts that I make at the start of each year, where I look at data, both macro and company-level. That is not true!

Since I am lucky enough to have access to databases that carry data on all publicly traded stocks, I choose all publicly traded companies, with a market price that exceeds zero, as my universe, for computing all statistics. Consequently, I do report industry averages for the two fastest growing emerging markets in India and China.

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. In the table below, we compare the changes in regional marketcapitalizations (in $ millions) over time.

A few years ago, I wrote a paper for practitioners on the cost of capital , where I described the cost of capital as the Swiss Army knife of finance, because of its many uses. Much of the confusion in applying cost of capital comes from not recognizing that it morphs, depending on where it is being used.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content