This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the world of finance and investing, the concept of beta plays a vital role in assessing an investment’s risk and volatility. Whether you’re a seasoned investor or new to the market, understanding beta can empower you to make informed decisions. What is beta and how do you calculate beta?

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. At the start of 2022, the ten sectors (US) with the highest and lowest relative risk (unlettered betas), are shown below.

Beta & Risk 1. Equity RiskPremiums 2. Book Value Multiples 3. Working capital needs Thus, I compute pricing multiples based on revenues (EV to Sales, Price to Sales), earnings (PE, PEG), book value (PBV, EV to Invested Capital) or cash flow proxies (EV to EBITDA). Return on Equity 1. Debt Details 1.

The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market riskpremium is calculated from a market rate of return less a risk-free rate. Therefore, the risks of the firm are eventually increased. Conclusion.

For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Price to Book 3. High-Low Price Risk Measure 5.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

It needs to incorporate both the project risk and the opportunity cost, typically done using the CAPM method. However, market information required for CAPM, such as beta coefficients and riskpremiums, may not be available for SMEs. Why not book your demo here to find out how Valutico can help you in valuing SMEs.

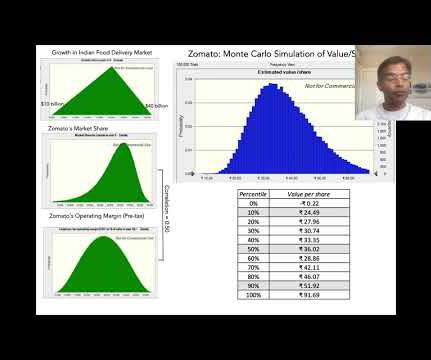

The second is the cost of capital, a number that most valuation classes and books (including mine) belabor to the point of diminishing returns. Finally, dismissing Zomato as an investment, just because it does not make money now, or fails to meet some conventional value tests on pricing (PE, Price to Book), is investing malpractice.

Rf = Risk-free Rate. B = Beta. (Rm Rm – Rf) = Equity Market RiskPremium. Cp = Cost of Equity Premium. DCF WACC—similar to the above except that it calculates a different WACC in each forecast period based on a changing capital structure (D/E) and thus a changing beta in each period. Cost of Debt.

He is member of the Beta Gamma Sigma Honor Society, Financial Executives International, and the National Association of Corporate Directors (NACD). Dr. Everett also has an M&A Advisory and business valuation practice. He specializes in the valuations of business enterprises and their intangible assets.

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. Book versus Market : The book debt ratio is built around using the accounting measure of equity, usually shareholder's equity, as the value of equity.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content