This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

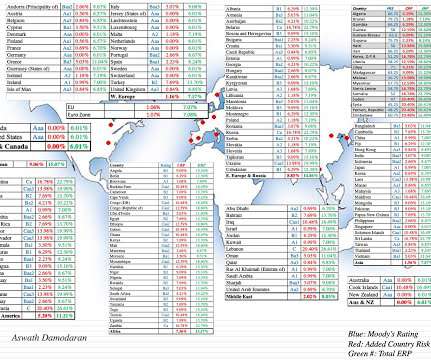

Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021).

The premium that investors demand over and above the riskfreerate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

Interest Rates and Inflation Inflation and interest rates are intertwined, and when their paths deviate, as they sometimes do, there is always a reckoning. Put simply, no central bank, no matter how powerful, can force market interest rates down, if inflation expectations stay low, or up, if investor are anticipating high inflation.

More importantly, we’ll dig deeper into how discount rates can influence investment choices and how they’re used to figure out a company’s worth. What is a discount rate? The “discount rate” does two main things. For central banks like the Federal Reserve, it helps control the economy.

For instance, assume a bank is performing a discounted cash flow analysis for a mortgage. If a bank expects a borrower to make mortgage payments before the contractual due dates, the prepayments would lead to a lower end value in the discounted cash flow calculation than if the payments were made per the contract terms.

In this section, I will begin measures of country default risk, including sovereign ratings and CDS spreads, before moving to more expansive measures of country risk before concluding with measures of equity riskpremiums for countries, a pre-requisite for estimating the values of companies with operations in those countries.

The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors. That view has never made sense, because central banking power over rates is at the margin, and the key fundamental drivers of rates are expected inflation and real growth.

Note that in all three cases, it is not the Fed that is driving rates, but what is happening to inflation. As the inflation bogeyman returns, the worries of what may need to happen to the economy to bring inflation back under control have also mounted.

A firm borrows from banks or bondholders and it has to pay the interest. The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market riskpremium is calculated from a market rate of return less a risk-freerate.

The first is that the Fed Funds rate is currently close to zero, limiting the Fed's capacity to signal with lower rates. for the year are at war with its concurrent promise to keep rates low; after all, adding those numbers up yields a intrinsic riskfreerate of 8.7%. Riskfree rate will rise.

But people who aim for investment banking roles are very much into those bells and whistles, so questions about the DDM and other “exotic” methodologies began rolling in. To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

In a sign of how volatile inflation expectations have been over the last year, I looked at the probabilities that the Federal Reserve Bank of St. Louis estimates for inflation rates exceeding 2.5% Consequently, as inflation increases, equity riskpremiums will tend to increase.

Investors in Saudi Arabia are still exposed to significant risks from political upheaval or unrest, and may prefer a more comprehensive measure of country risk. For three decades, I have wrestled with measuring this additional risk exposure and converting that measurement into an equity riskpremium, but it remains a work in progress.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies. Thus, if the US treasury bond rate (4.5%) is the riskfree rate in US dollars, and the expected inflation rates in US dollars and Brazilian reals are 2.5%

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content