This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The premium that investors demand over and above the risk free rate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact.

In this section, I will begin measures of country default risk, including sovereign ratings and CDS spreads, before moving to more expansive measures of country risk before concluding with measures of equity riskpremiums for countries, a pre-requisite for estimating the values of companies with operations in those countries.

Equity RiskPremium Path : The equity riskpremium of 5.24%, estimated at the start of May 2022, is at the high end of historical equity riskpremiums , but we have seen higher premiums, either in crises (end of 2008, first quarter of 2020) or when inflation has been high (the late 1970s).

And Consequences If you are wondering why you should care about risk capital's ebbs and flows, it is because you will feel its effects in almost everything you do in investing and business. The 2008 banking and market crisis caused a drop of almost 50% in 2009, and it took the market almost five years to return to pre-crisis levels.

Exacerbating the pain, corporate default spreads rose during the course of 2022: While default spreads rose across ratings classes, the rise was much more pronounced for the lowest ratings classes, part of a bigger story about risk capital that spilled across markets and asset classes.

For central banks like the Federal Reserve, it helps control the economy. They set this rate to affect how much money moves through banks and influences short-term interest rates. We are going to focus on how discount rates are used in the context of investment, rather than in the context of central banks.

Just as rising equity riskpremiums push up the cost of equity, rising default spreads push up the cost of debt of companies, with the added complication of higher default risk for those companies that had pushed to the limits of their borrowing capacity in a low interest-rate environment.

In leveraged buyouts (LBOs), a private equity (PE) sponsor acquires controlling ownership of a target company, typically by using a significant amount of bank loans. In a new study, we focus on a controversial issue: Many PE sponsors have prior relationships with law firms representing banks in LBO loan negotiations.

For instance, assume a bank is performing a discounted cash flow analysis for a mortgage. If a bank expects a borrower to make mortgage payments before the contractual due dates, the prepayments would lead to a lower end value in the discounted cash flow calculation than if the payments were made per the contract terms.

While we have increasingly given central banks primacy in discussions of interest rates, it remains my view that markets set rates, and while central banks can nudge market expectations, they cannot alter them. Connecting this linkage to the discussion of US inflation in the prior sections, here are the takeaways.

Investors will either see more relative risk (or beta) in these companies, if the risks affect an entire sector, or in equity riskpremiums, if they are market-wide. Applications : My argument for using implied equity riskpremiums is that they are dynamic and forward-looking. at the end of 2007 to 0.85

But people who aim for investment banking roles are very much into those bells and whistles, so questions about the DDM and other “exotic” methodologies began rolling in. To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology.

Further to our prior post about Delaware’s two new appraisal decisions, SWS Group was a small, struggling bank holding company that merged on January 1, 2015 into one of its own substantial creditors, Hilltop Holdings. Stockholders of SWS received a mix of cash and Hilltop stock worth $6.92 at closing. below the merger price.

A firm borrows from banks or bondholders and it has to pay the interest. The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market riskpremium is calculated from a market rate of return less a risk-free rate.

We note that the higher the expected rate (in other words, the greater the risk is perceived as necessary, to the point of requiring a substantial "riskpremium"), the lower the multiple that will apply and therefore the lower valuation: we buy cheaper which is less safe. 11% per year. 10% per year. around 1.5%). -

The second and more powerful factor is that the reason that a central bank is able to signal to markets, only if it has credibility, since the signal is more about what the Fed sees, using data that only it might have, about inflation and real growth in the future. Riskpremiums No effect or even a decrease.

Dr. Everett is the author of the children’s financial literacy thriller Toby Gold and the Secret Fortune, which incorporates such financial topics as saving, investing, banking, entrepreneurship, interest rates, return on investment, and net worth. Everett He holds a Ph.D. in Quantitative Economics from Tufts University. Petersburg, Russia.

In computing this implied equity riskpremium for the S&P 500, I start with the dividends and buybacks on the stocks in the index in the most recent year (which is known) and assume that they grow at the rate that analysts who follow the index are projecting for the next five years.

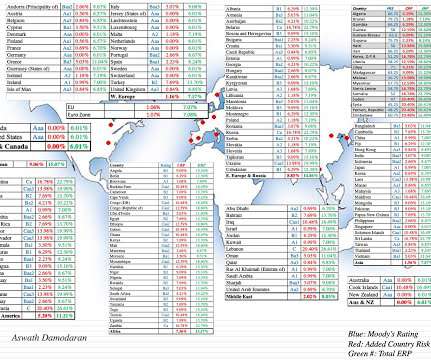

Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equity riskpremiums , I described the equity riskpremium as the additional return you would demand, over and above the risk free rate.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. against developed market currencies.

In a sign of how volatile inflation expectations have been over the last year, I looked at the probabilities that the Federal Reserve Bank of St. Consequently, as inflation increases, equity riskpremiums will tend to increase. Louis estimates for inflation rates exceeding 2.5%

The second is that there are great (and free) sources for macro economic data, ranging from the Federal Reserve (FRED) to the World Bank and I don’t see the point of replicating something that they already do well.

Note that this framework applies for all businesses, from the smallest, privately owned businesses, where debt takes the form of bank loans and even credit card borrowing and equity is owner savings, the largest publicly traded companies, where debt can be in the form of corporate bonds and equity is shares held by public market investors.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). The rate would be calculated based on a 10-year "risk-free interest" rate depending on the currency, increased by a 1% riskpremium (1.5%

If these ESG revisionists are to be believed, if companies had adopted ESG early enough, there would have been no banking crisis in 2008, and if investors had screened stocks for ESG quality, they would not have lost money in the corporate scandals and meltdowns of the last decade.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

Investors in Saudi Arabia are still exposed to significant risks from political upheaval or unrest, and may prefer a more comprehensive measure of country risk. For three decades, I have wrestled with measuring this additional risk exposure and converting that measurement into an equity riskpremium, but it remains a work in progress.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

During his campaign, Argentine President Javier Milei promised to close the countrys central bank and adopt the dollar as the countrys currency. The main attraction of full dollarization is the elimination of the risk of a sudden, sharp devaluation of the countrys exchange rate, the IMF writers point out. from 2004-2007.

NYU Business School Professor Damoradans widely used valuation data, for example, currently shows the United States as having among the lowest equity riskpremiums in the world. [3] Bank of England Working Paper (2020). In the United States, the cost of capital is lower than elsewhere. 2] SEC website ( [link] ). [3] 3] [link].

Healy before the Subcommittee on Banking and Currency on Wagner-Lea Act, S. Investment companies have been compelled to finance banking clients of the insiders and companies in which they were personally interested. at 25) and they hold more of their wealth in regulated funds, as opposed to bank products, than Europe or Japan ( id.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

The table below computes debt to capital ratios, in book and market terms, by sector and sub-region: I would begin by separating the financial sector from the rest of the market, since debt to banks is raw material, not a source of capital. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks!

The Risk Effect There are emerging markets that have delivered higher returns than developed markets, but in keeping with a core truth in investing and business, these higher returns often go hand-in-hand with higher risk. The answers, to you, may seem obvious, but I find it useful to organize the obvious into buckets for analysis.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. In the table below, I show my estimates of the implied equity riskpremium for the S&P 500 at the start of every month, since January 2024, and on March 14, 2025.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content