This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Looking ahead to 2023, with risk-freerates and credit spreads still elevated and the credit, deal making, regulatory and geopolitical environments uncertain, corporate borrowers and sponsors will need to plan rigorously to succeed on levered acquisitions and spin-offs and important refinancings. over the same period.

As a long-time skeptic about the Fed’s (or any Central Bank’s) capacity to alter much in markets or the economy, I decided now would be as good a time as any to confront some widely held beliefs about central banking powers, and counter them with data.

Traditionally, if someone asked the “ sales & trading vs. investment banking ” question, the response was easy: “Do banking unless you really, really like trading and could not imagine doing anything else.”. Investment Banking: 13%. Credit Investing or Credit Rating Agency: 6%. Mixed IB / S&T Background: 6%.

Interest Rates and Inflation Inflation and interest rates are intertwined, and when their paths deviate, as they sometimes do, there is always a reckoning. Put simply, no central bank, no matter how powerful, can force market interest rates down, if inflation expectations stay low, or up, if investor are anticipating high inflation.

More importantly, we’ll dig deeper into how discount rates can influence investment choices and how they’re used to figure out a company’s worth. What is a discount rate? The “discount rate” does two main things. For central banks like the Federal Reserve, it helps control the economy.

Returns in 2022 In my first classes in finance, as a student, I was taught that the US treasury rate was a riskfreerate, with the logic being that since the US treasury could always print money, it would not default. I will wager that you would have seen rates go up, with or without the Fed.

For instance, assume a bank is performing a discounted cash flow analysis for a mortgage. If a bank expects a borrower to make mortgage payments before the contractual due dates, the prepayments would lead to a lower end value in the discounted cash flow calculation than if the payments were made per the contract terms.

The first is that the Fed Funds rate is currently close to zero, limiting the Fed's capacity to signal with lower rates. for the year are at war with its concurrent promise to keep rates low; after all, adding those numbers up yields a intrinsic riskfreerate of 8.7%. for 2021 and inflation of 2.2%

A firm borrows from banks or bondholders and it has to pay the interest. The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market risk premium is calculated from a market rate of return less a risk-freerate.

That said, when investors buy equities, it would be both irrational and illogical to settle for expected returns that are less than what you can earn on riskfree or guaranteed investments, though behavioral finance suggests that both irrationality and illogic are persistent human traits. Stocks: The What Next?

For the right person, though, fixed income research can be even better than equity research, whether you’re at a bank, an asset management firm, a hedge fund, or a credit rating agency: Table of Contents: What is Fixed Income Research? Rates: Is the “risk-freerate” truly risk-free ?

But people who aim for investment banking roles are very much into those bells and whistles, so questions about the DDM and other “exotic” methodologies began rolling in. To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology.

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM).

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM).

The WACC formula derives the current cost of each form of finance, starting with the risk-freerate, the expected return on equity, and the costs associated with debt financing. The required rate of return for equity (Re) is generally calculated using the Capital Asset Pricing Model (CAPM).

At the other end, in perhaps the most malignant scenario, titled T he Seventies Show , inflation continues to rise, even as the economy goes into recession and risk premiums spike, leading to a further correction of close to 50% in the market.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

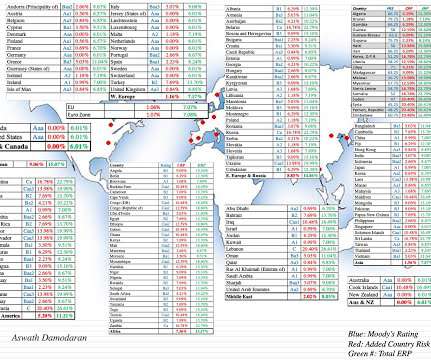

The conventional practice, when estimating riskfreerates, has been to use the government bond rate in the local currency, if available, as the riskfree rate in that currency, and that practice is wrong when markets perceive default risk in the sovereign and build that into the government bond rate.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021).

Country Risk: Currency and Cost of Capital As a final part to this post, to see the shifts in country risk that we have seen in 2022, let’s start with an assessment of riskfreerates.

Monetary policy across major markets, including the pace and timing of interest rate cuts by major central banks will have a material impact on risk-freerates, a key input for valuations across multiple asset classes.

In my last three posts, I looked at the macro (equity risk premiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

In a sign of how volatile inflation expectations have been over the last year, I looked at the probabilities that the Federal Reserve Bank of St. Louis estimates for inflation rates exceeding 2.5% Embedded in this picture are the multiple pathways that inflation, expected and unexpected, can affect the the values of businesses.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

Investors in Saudi Arabia are still exposed to significant risks from political upheaval or unrest, and may prefer a more comprehensive measure of country risk.

I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies. Thus, if the US treasury bond rate (4.5%) is the riskfree rate in US dollars, and the expected inflation rates in US dollars and Brazilian reals are 2.5%

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content