This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I also used the banking framework to argue that good banks have stickier deposits, with a higher precent of these deposits being non-interest bearing, that they invest in loans and investment securities on which they earn interest rates that cover and exceed the default risk in these investments. All Equity, All the time!

That does not surprise me, since I have never bought into the “Fed did it” theme, and have written multiple posts about why it is inflation and economic growth that drive interest rates, not central banks. trillion in market value in the first six months in the year , but the severity of last year's decline has still left them $14.4

While we have increasingly given central banks primacy in discussions of interest rates, it remains my view that markets set rates, and while central banks can nudge market expectations, they cannot alter them. Connecting this linkage to the discussion of US inflation in the prior sections, here are the takeaways.

The table below summarizes the market cap change, by region of the world: It is no surprise that Eastern Europe and Russia, which are in the eye of the hurricane, have seen the most damage to equities, but other than the Middle East, every other equity market in the world is down, with the US, EU and China shedding significant marketcapitalization.

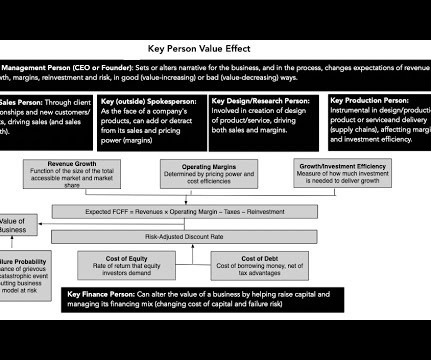

In businesses like banking, consulting or the law, rainmakers can represent a significant portion of value, and their departure can be not just damaging but catastrophic. The value added by a superstar trader will be greater if he or she works at a ten-person trading group than if they work at a large investment bank.

Consider, for instance, an investor who picks stocks based upon price to book ratios, who finds a stock trading at a price to book ratio of 1.5. While some of the companies in this data trace their existence back decades, there is a healthy proportion of younger companies, many in emerging markets and new industries.

The second and more powerful factor is that the reason that a central bank is able to signal to markets, only if it has credibility, since the signal is more about what the Fed sees, using data that only it might have, about inflation and real growth in the future.

I do believe that too much is often made of these differences, as it is generally more the rule than the exception that markets, when they are up strongly, get the bulk of that rise from a small sub-set of stocks or sectors. The results are similar if you break stocks down based upon price to book ratios or revenue growth rates.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like marketcapitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content