This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. Stocks: The What?

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact.

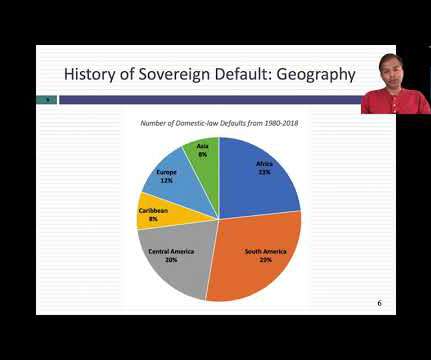

In the month since, I have added two more data updates, one on US equities and one on interest rates , but my attention was drawn away by other interesting stories. Default Risk As with individuals and businesses, governments (sovereigns) borrow money and sometimes struggle to pay them back, leading to to the specter of sovereign default.

Investment Consequences As the storm clouds of higher inflation and interest rates, in conjunction with slower or even negative economic growth, gather, it should come as no surprise that equity markets are struggling to find their footing. At the close of trading on May 5, 2022, the S&P 500 stood at 4147, down 13.3%

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. trillion below their values from the start of 2022. that was lost last year.

In leveraged buyouts (LBOs), a private equity (PE) sponsor acquires controlling ownership of a target company, typically by using a significant amount of bank loans. In a new study, we focus on a controversial issue: Many PE sponsors have prior relationships with law firms representing banks in LBO loan negotiations.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. Historical Context In my earlier post, I noted that US equity market performance in 2022 made it the seventh worst year in stock market history, if you go back to 1928.

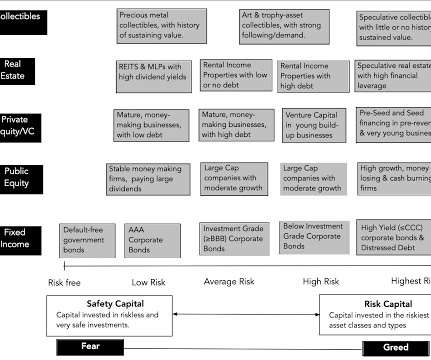

And Consequences If you are wondering why you should care about risk capital's ebbs and flows, it is because you will feel its effects in almost everything you do in investing and business. The 2008 banking and market crisis caused a drop of almost 50% in 2009, and it took the market almost five years to return to pre-crisis levels.

For central banks like the Federal Reserve, it helps control the economy. They set this rate to affect how much money moves through banks and influences short-term interest rates. The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. Those rates stayed low through the rest of 2020, even as equity markets recovered and corporate bond spreads fell back to pre-crisis levels. Riskpremiums No effect or even a decrease.

While we have increasingly given central banks primacy in discussions of interest rates, it remains my view that markets set rates, and while central banks can nudge market expectations, they cannot alter them.

But people who aim for investment banking roles are very much into those bells and whistles, so questions about the DDM and other “exotic” methodologies began rolling in. To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology.

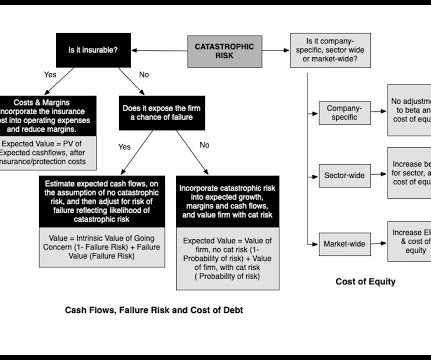

Minuses : As in the last approach, you still have to estimate a probability that a catastrophe will occur, and in addition, and there can be challenges in estimating the value of a business, if the company fails in the face of catastrophic risk. 4 & 5 Uninsurable Risk. Note that these higher discount rates apply in both scenarios.

A firm uses a mix of equity and debt to minimize the cost of capital. In general, the cost of debt is lower than the cost of equity due to the tax advantage of debt. A firm borrows from banks or bondholders and it has to pay the interest. The popular method to find the cost of equity is the Capital Asset Pricing Model (CAPM).

Further to our prior post about Delaware’s two new appraisal decisions, SWS Group was a small, struggling bank holding company that merged on January 1, 2015 into one of its own substantial creditors, Hilltop Holdings. Stockholders of SWS received a mix of cash and Hilltop stock worth $6.92 at closing. below the merger price.

If equity markets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equity markets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

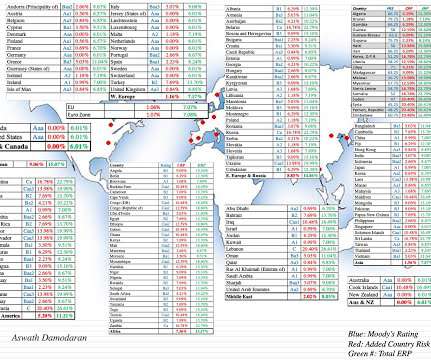

Country Risk: EquityRisk For equity investors, the price of risk is captured by the equityriskpremium, and equityriskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

Dr. Everett is the author of the children’s financial literacy thriller Toby Gold and the Secret Fortune, which incorporates such financial topics as saving, investing, banking, entrepreneurship, interest rates, return on investment, and net worth. Everett He holds a Ph.D. in Quantitative Economics from Tufts University. Petersburg, Russia.

In my last post , I described the wild ride that the price of risk took in 2020, with equityriskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equityriskpremiums , I described the equityriskpremium as the additional return you would demand, over and above the risk free rate.

To fund the business, you can either use borrowed money (debt) or owner's funds (equity), and while both are sources of capital, they represent different claims on the business. Even government-owned businesses fall under its umbrella, with the key difference being that equity is provided by the taxpayers.

In my last three posts, I looked at the macro (equityriskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

In this section, I will begin by looking at the bond market effects and then move on to equities and other asset classes, starting by looking at the localized reaction (for Ukranian and Russian securities) and then the global ripple effects. As Russian equities have imploded, the ripple effects again are being felt across the globe.

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). DEBRA Proposal (« Debt-Equity Bias Reduction Allowance). DEBRA Proposal (« Debt-Equity Bias Reduction Allowance). Two major axes.

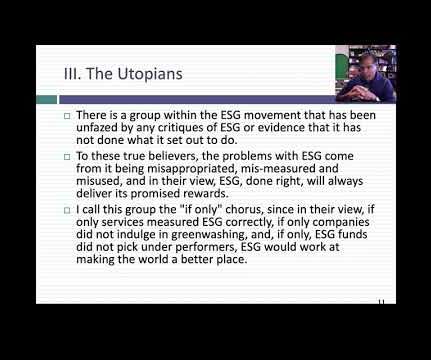

If these ESG revisionists are to be believed, if companies had adopted ESG early enough, there would have been no banking crisis in 2008, and if investors had screened stocks for ESG quality, they would not have lost money in the corporate scandals and meltdowns of the last decade.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

Investors in Saudi Arabia are still exposed to significant risks from political upheaval or unrest, and may prefer a more comprehensive measure of country risk. For three decades, I have wrestled with measuring this additional risk exposure and converting that measurement into an equityriskpremium, but it remains a work in progress.

Thus, as you peruse my historical data on implied equityriskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

Thus, my estimates of equityriskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. That said, to value companies today, I have no choice but to bring in the economics and politics of the world that these companies inhabit.

Strong empirical evidence shows the United States has a lower cost of equity capital than comparable countries and that this lower cost is attributable in part to an institutional design that protects the independence of securities regulators and assures strong enforcement. Bank of England Working Paper (2020). 3] [link]. [4]

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equityriskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

The Debt Trade off As a prelude to examining the debt and equity tradeoff, it is best to first nail down what distinguishes the two sources of capital. To me, the key distinction between debt and equity lies in the nature of the claims that its holders have on cash flows from the business.

The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market. That process of risk analysis and estimating riskpremiums starts by understanding why some countries are riskier than others.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content