This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I also used the banking framework to argue that good banks have stickier deposits, with a higher precent of these deposits being non-interest bearing, that they invest in loans and investment securities on which they earn interest rates that cover and exceed the default risk in these investments. All Equity, All the time!

The plan by the Big Three banks to unwind their cross-shareholdings points to a long-awaited turn to better corporate governance. As such, the big banks’ pledges suggest that Japanese business is taking the need for change seriously, Wu says. The announcements in June by Japan’s three megabanks that they will sell $5.4

While we have increasingly given central banks primacy in discussions of interest rates, it remains my view that markets set rates, and while central banks can nudge market expectations, they cannot alter them.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. US Equities in 2023: Into the Weeds! that was lost last year.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. Those rates stayed low through the rest of 2020, even as equity markets recovered and corporate bond spreads fell back to pre-crisis levels. to close to zero, and the ten-year T.Bond rate declining to close to 0.70%.

These interviews are not just a mere formality but a critical component of the hiring process in finance, investment banking, and consulting. Understanding the Concept: In essence, FCFF encapsulates the cash that can be distributed to both debt and equity holders after meeting operational needs and capital expenditures.

Analysts use financial metrics and multiples such as Price to Earnings (P/E), Price to Book (P/B), Enterprise Value to Sales (EV/Sales), Enterprise Value to EBITDA (EV/EBITDA), and Price to Book (P/B) ratios derived from trading data of similar public companies or deal pricing data of similar M&A transactions.

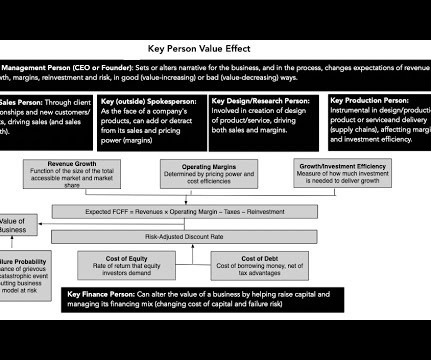

In businesses like banking, consulting or the law, rainmakers can represent a significant portion of value, and their departure can be not just damaging but catastrophic. The value added by a superstar trader will be greater if he or she works at a ten-person trading group than if they work at a large investment bank.

In this post, I will begin with a historical assessment of stock returns in the recent past, then move on to evaluate the returns that investors can expect to make, given how they are priced at the start of 2022, and end with a do-it-yourself valuation of the index right now. The year that was.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

In this section, I will begin by looking at the bond market effects and then move on to equities and other asset classes, starting by looking at the localized reaction (for Ukranian and Russian securities) and then the global ripple effects. As Russian equities have imploded, the ripple effects again are being felt across the globe.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

Adani's Debt Load The investment side of the Adani story is not complete without bringing in the financing part, since the money for these investments has to come from somewhere, either internally, residual cash flows from existing operations, or externally, from new debt or equity.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content