This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On the heels of several history-making bank collapses in the first quarter of 2023, financial institutions must fortify their internal controls programs to respond to greater scrutiny from federal regulators. Areas where banks are expected to face stricter rules and supervision include: Stress test models and contingency planning.

AuditBoard and RSM’s new ebook, Third-Party Risk Management: Trends and Strategies to Help You Stay Ahead of the Curve, translates current TPRM trends and lessons learned into actionable ideas to help your organization identify, reduce, and monitor third-party risk. banking disruptions, ESG, new regulations, etc.),

Keeping up with regulatory change impacts retail community banks complying with the FDIC Improvement Act (FDICIA), bank holding companies complying with the Comprehensive Capital Analysis and Review (CCAR) and Dodd-Frank Stress Testing (DFAST), and securities broker-dealers reporting to the Financial Industry Regulatory Authority (FINRA).

Further, it can be fraught with complexity due to the high volume of transactions, multiple integrated systems, banks, and payment types — leading to an increase in opportunity and incentive for fraud. Banking payment and positive pay systems. Operating cost. Supply chain risk and operating efficiencies. Supplier/vendor master file.

For more guidance on how to calculate the true cost of capital, download our eBook: Finding the Right Financing for Your Capital Needs. What other controls or covenants will the lender require?

Relevant public interest entities such as insurance or banking companies with 500+ employees. Limited Liability Partnerships (LLPs) which include: Traded or banking LLPs with 500+ employees.

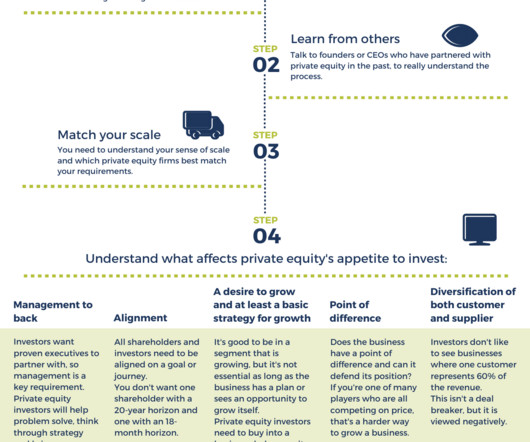

In our ebook Stakeholders in Your Business , guest contributor Gareth Banks from Champ Ventures explained how private equity works and what sort of opportunities private equity investors look for. We have distilled some of Gareth’s advice down into this cheat sheet, to help you make your business private equity ready.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content