This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This article will focus on careers and recruiting , while the accompanying YouTube video will discuss the technical/modeling aspects in more detail. We don’t have space in this article to cover technical questions, but we may publish a separate feature on this topic.

If you want to read to a step-by-step example of a DCF, skip to the end of the article here. Well, the short answer is after that forecast period where we estimate each year’s cash flows then discount them, we add a single number at the end to account for all the theoretical years in the future, called the TerminalValue (TV).

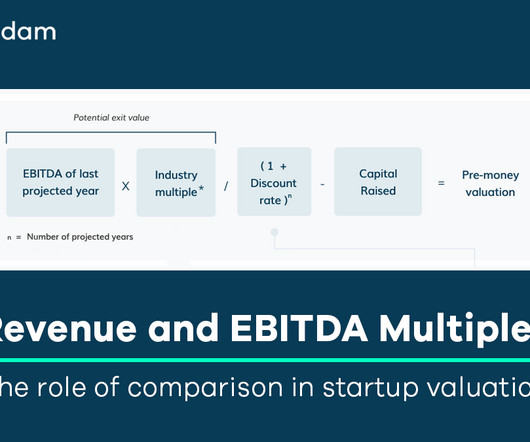

Specifically, in understanding the exit potential of a company, by applying a multiple to the terminalvalue (the last year’s projected EBITDA or revenue). You can read more about our benchmarking with multiples in the associated helpdesk article , where we’ve also published some more detail on the reference multiples we use.

Documents to consider may include partnership agreements, articles of incorporation, bylaws, operating agreements, buy-sell agreements, investment letter stock restrictions, option agreements, lock-up requirements or others that may be relevant. Paragraph 8 above, with its sub-paragraphs a.

This article is your comprehensive guide to mastering the art of answering the top 29 valuation interview questions. Can TerminalValue be Negative? Navigating Theoretical and Practical Aspects: Theoretical scenarios where terminalvalue might be negative can be explored by considering the perpetuity growth method.

This article aims to provide you with a comprehensive guide on how to value a company, covering different valuation methods, financial analysis, and qualitative factors. Understanding Company Valuation Definition of Company Valuation: Company valuation is the process of determining the economic value of a business entity.

How to Value an SME—An Introductory Guide Small and Medium-sized Enterprises (SMEs) are key players in driving economic growth, fostering innovation, and creating jobs. In this article, we’ll unravel how to value SMEs, including what you need to consider to do so accurately. How do I value an SME?

This article explores the pros and cons of the DCF method and sheds light on its utility in the financial world. Outline of the Article H1: Introduction What is the Discounted Cash Flow (DCF) method? Any inaccuracies in the inputs, such as revenue forecasts, discount rates, or terminalvalues, can lead to misleading valuations.

Most articles are copied/pasted/tweaked text, others appear to be written by ChatGPT, and others repeat generic questions you might get in an interview for a janitorial position. A: See our guide and examples for the “ Walk me through your resume ” question and the article on how to walk through your resume in buy-side interviews.

These multiples are applied to target company’s latest financials such as revenue, earnings and book value of equity to arrive at an estimate of enterprise value or equity value. For more insights, do have a look at our article on market multiple based valuation.

I addressed the question in an article in the Business Valuation Review of the American Society of Appraisers in 1994. I have addressed this issue in several books and numerous articles and blog posts since then. The answer to the questions was, and still is, of course, no.

In this article, we’ll assume that there are 5 major verticals within oil & gas: Exploration & Production (E&P or “Upstream”) – These companies explore and drill for oil and gas in different locations; once they find deposits, they produce the energy. Essentially, the NAV Model is a super-long-term DCF without a TerminalValue.

I think this is a bit too complicated, so this article will use these 3 categories: Base Metals and Bulk Commodities – Anything used for energy (coal), as a precursor to other metals (iron ore), or to produce electronics, batteries, and other products (copper, cobalt, lithium, aluminum, etc.)

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content