This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Share Price Performance KHC’s heavy debt load following its merger in 2015 was lightened by the pandemic’s increased demand for food, lower interest costs, and opportunities for divestment. Despite a flat operating performance in 2021, the company successfully reduced its netdebt to $22 billion. billion to USD 74.5

Share Price Performance KHC’s heavy debt load following its merger in 2015 was lightened by the pandemic’s increased demand for food, lower interest costs, and opportunities for divestment. Despite a flat operating performance in 2021, the company successfully reduced its netdebt to $22 billion. billion to USD 74.5

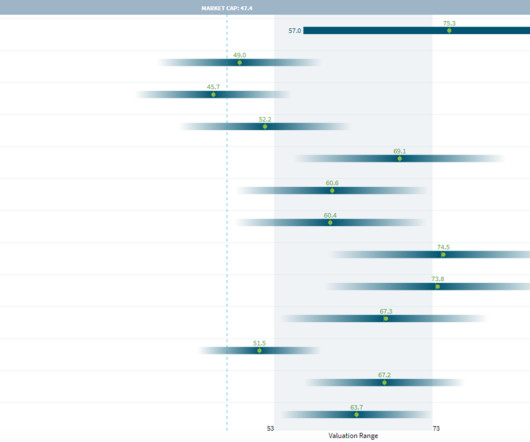

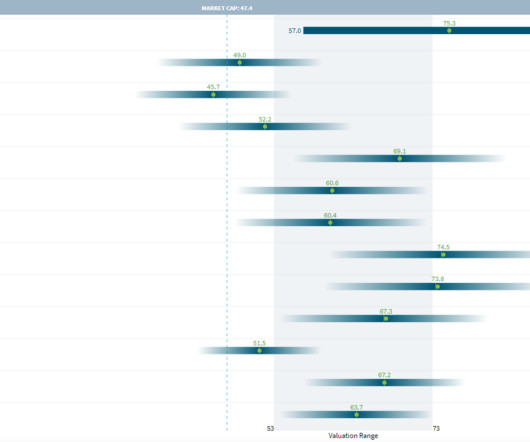

Compared with last year’s net income of GBP 10.3 (USD billion in netdebt, reducing total debt to GBP 17.5 (USD The Trading Comparables analysis resulted in a valuation range of GBP 98 (USD 199) billion to GBP 137 (USD 166) billion by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B.

Net assets have fallen in 2020 after selling UD truck segment to Isuzu Motors. However, increased CAPEX for capacity expansion and battery development lead to increase in net fixed assets again. In 2020, its net-debt to equity ratio stood at 0.9x. EBIT margin expansion in 21E likely to stay. Ratios – Volvo.

The company has almost no long-term debt, thought is does have short term debt, leading to a negative netdebt-to-equity ratio of 0.7x. EBIT margin on a slightly lower level given an increase of low-cost manufacturers. The author(s) cannot be held liable for any actions taken as a result of reading this article.

In this article we explore some of the main valuation methods, including when to adopt them. For a thorough description and explanation of a DCF, see our full DCF article here. A lower EV/EBIT ratio indicates a potentially better value for investors. So, what are the main company valuation methods?

A quick Google search will reveal numerous articles about each of these cases, so I won’t retread old ground here. In particular, IBP’s past performance revealed strong swings in annual EBIT and net earnings. 3841 (VCL) (Del. 29 2008) , and. Osram Sylvania, Inc. Townsend Ventures, LLC , C.A. 8123-VCP (Del.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content