This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

EBIT and EBITDA are two measurements of business profitability. This article will discuss two accounting terms used to build the FCFF - EBIT and EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). Both EBIT and EBITDA are indicators of the firm's profitability. . What is EBIT? What is EBITDA?

If you’re interested in selling your business, you may be doing some research on how businesses are valued. There are lots of misleading theories out there about how to best value a business, including using a multiple of revenue (not good) or a multiple of net profit (even worse).

billion with EBIT margin increasing to 16.6% The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. Sales rose 5% to CHF 7.1

billion with EBIT margin increasing to 16.6% The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. Sales rose 5% to CHF 7.1

EBIT margin is likely to expand significantly through better cost control. We see an EBIT margin around 15% as a maximum for this Ralph Lauren. The author(s) cannot be held liable for any actions taken as a result of reading this article. After the revenue rebound in 22E, we assume revenue growth to normalize.

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT, P/E and P/B. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of CAD 14.7 billion using a WACC of 8.8%. billion to CAD 28.1

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. billion we suggest that the company is fairly valued Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of USD 27.1

The Trading Comparables analysis resulted in a valuation range of $257 billion to $296 billion by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. Link to valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. Let us know in the comments.

The Trading Comparables analysis resulted in a valuation range of $81 to $158 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of $99.5 Link to detailed valuation.

The Trading Comparables analysis resulted in a valuation range of $81 to $158 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of $99.5 Link to detailed valuation.

EBIT margin expansion in 22E probably only short-lived. Going forward, we see the EBIT margin to range between 7-8%. The author(s) cannot be held liable for any actions taken as a result of reading this article. After the revenue rebound in 22E, we assume revenue growth to normalize. Long-term share price performance potential.

billion to USD 108 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the analisys Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of USD 212 billion using a WACC of 6.8%.

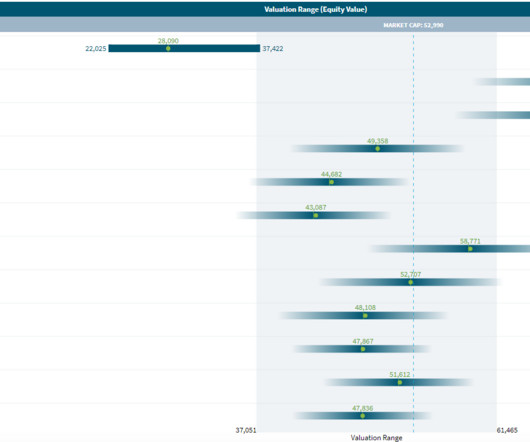

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of USD 28.09 billion using a WACC of 11.3%. billion to USD 71.14

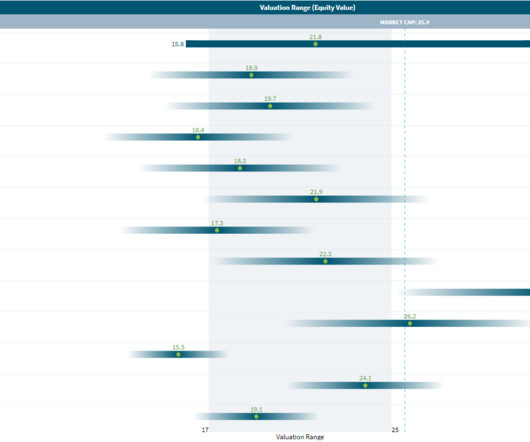

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of USD 21.8 billion using a WACC of 10%. billion to USD 32.3

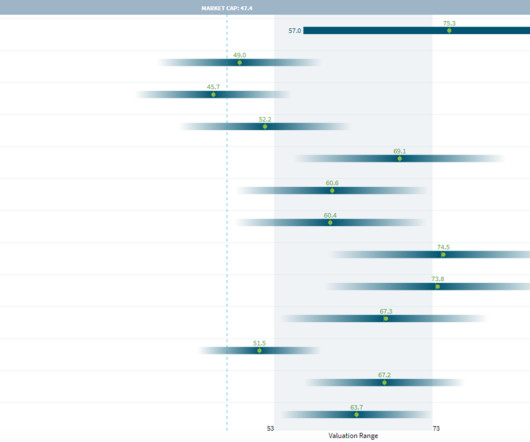

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of USD 75.3 billion using a WACC of 6.3%. billion to USD 74.5

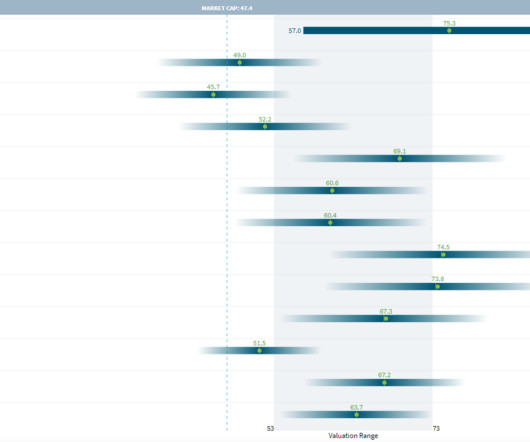

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of USD 75.3 billion using a WACC of 6.3%. billion to USD 74.5

The Trading Comparables analysis resulted in a valuation range of €305 billion to €492 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. Let us know in the comments.

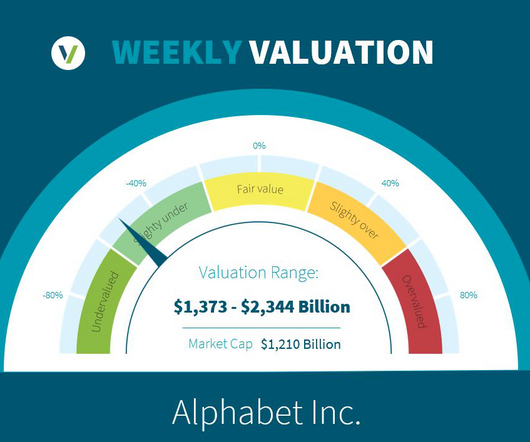

The Trading Comparables analysis resulted in a valuation range of $1,517 billion to $2,344 billion by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. Link to valuation Disclaimer This article is for informational purposes only and does not constitute investment advice.

The Trading Comparables analysis resulted in a valuation range of $121 billion to $150 billion by applying the observed trading multiples EV/EBITDA and EV/EBIT. Link to valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. The DCF analysis produced a value of $93.5

The Trading Comparables analysis resulted in a valuation range of $83 billion to $118 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of $68.6 Link to valuation.

The Trading Comparables analysis resulted in a valuation range of $202 billion to $231 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. Link to valuation. Disclaimer.

The Trading Comparables analysis resulted in a valuation range of $83 billion to $118 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Discounted Cash Flow analysis produced a value of $68.6 Link to valuation.

The Trading Comparables analysis resulted in a valuation range of $202 billion to $231 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. Link to valuation. Disclaimer.

In practice, professionals rely on several results, assessed at different levels of the income statement: - the gross operating surplus (EBIT or EBITDA) - net operating surplus (ENE or EBIT) - the Current Result Before Tax (RCAI) - Net Income (NR) - Self-Financing Capacity (CAF) or operating cash flow. EBITDA and EBIT).

If it can maintain a 6-7% EBIT margin it changes the market’s assessment of the company. If it can maintain a 6-7% EBIT margin, then this could be a catalyst for share price performance. The author(s) cannot be held liable for any actions taken as a result of reading this article. Reducing reliance on global supply chains.

The Trading Comparables analysis resulted in a valuation range of USD 503 billion to USD 812 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. Microsoft Corporation.

The Trading Comparables analysis resulted in a valuation range of USD 60 billion to USD 277 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. and Cisco Systems, Inc.

The Trading Comparables analysis resulted in a valuation range of USD 106 billion to USD 235 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Link to the valuation Disclaimer This article is for informational purposes only and does not constitute investment advice. and Alphabet Inc.

The Trading Comparables analysis resulted in a valuation range of GBP 98 (USD 199) billion to GBP 137 (USD 166) billion by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. Link to valuation Disclaimer This article is for informational purposes only and does not constitute investment advice.

billion to HKD 3,905 (USD 501) billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Trading Comparables analysis resulted in a valuation range of HKD 1,752 (USD 221.5) billion to HKD 3,905 (USD 501) billion.

We came up with this valuation range by using the observed trading multiples EV/EBITDA, EV/EBIT and P/E of peers such as Nike and Puma. . This article is for informational purposes only and does not constitute investment advice. billion and €26.2 By combining these two approaches we arrive at a fairly wide valuation range of €15.6

Our Trading Comparables analysis produced a valuation range of €178 billion to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. This article is for informational purposes only and does not constitute investment advice. Link to detailed valuation. Disclaimer.

The Trading Comparables analysis resulted in a valuation range of €98 to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. For our Trading Comparables we selected similar peers such as Heineken and Carlsberg.

billion to HKD 3,905 (USD 501) billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Trading Comparables analysis resulted in a valuation range of HKD 1,752 (USD 221.5) billion to HKD 3,905 (USD 501) billion.

billion to HKD 3,905 (USD 501) billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. The Trading Comparables analysis resulted in a valuation range of HKD 1,752 (USD 221.5) billion to HKD 3,905 (USD 501) billion.

The Trading Comparables analysis resulted in a valuation range of €98 to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. This article is for informational purposes only and does not constitute investment advice. For our Trading Comparables we selected similar peers such as Heineken and Carlsberg.

Our Trading Comparables analysis produced a valuation range of €178 billion to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. This article is for informational purposes only and does not constitute investment advice. Link to detailed valuation. Disclaimer.

We came up with this valuation range by using the observed trading multiples EV/EBITDA, EV/EBIT and P/E of peers such as Nike and Puma. . This article is for informational purposes only and does not constitute investment advice. billion and €26.2 By combining these two approaches we arrive at a fairly wide valuation range of €15.6

We used the observed trading multiples EV/EBITDA, EV/EBIT and P/E of a group of similar listed peers for our Trading Comparables analysis, arriving at a valuation range of $193 billion to $237 billion. This article is for informational purposes only and does not constitute investment advice. Let us know in the comments below.

Our Trading Comparables analysis, using the multiples EV/EBITDA, EV/EBIT and P/E, indicates a value range of PLN 5 billion ($1 billio n) to PLN 9 ($1.9 This article is for informational purposes only and does not constitute investment advice. Our DCF WACC analysis resulted in a valuation of PLN 10.7 billion ($2.2 billion ($2.2

billion to USD 150 billion, by utilizing observed metrics such as EV/EBITDA, EV/EBIT, and P/E ratios. Disclaimer This article is for informational purposes only and does not constitute investment advice. The DCF analysis yielded an equity value of USD 125 billion, predicated on a WACC of 10.1%. Youtube), Apple Inc.

Additionally, the Trading Comparables analysis generated a v aluation range of USD 220 billion to USD 290 billion, by utilizing observed metrics such as EV/EBITDA, EV/EBIT, and P/E ratios. Disclaimer This article is for informational purposes only and does not constitute investment advice.

Competitors like VW and GM only achieve EBIT margin between 5 and 7%. The author(s) cannot be held liable for any actions taken as a result of reading this article. The company targets to keep its ROE around 10% (with the help of its buyback program). Toyota is among the most consistent and most profitable car makers in the world.

EBIT margin expansion in 21E likely to stay. The author(s) cannot be held liable for any actions taken as a result of reading this article. I expect dividend yield over the near-term to range between 2.5-3.5%. Ratios – Volvo. After the revenue rebound in 22E, we assume revenue growth to normalize. Free cash flow – Volvo.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content