This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

’ Exactly why does the appraisers fee, which is independent of the amc total ‘appraisal services fee’, get to be disclosed as co mingled with the amc fee as one lump sum fee? In reply to Russell. Please allow me to introduce you to the concept of consumer protection. ‘The fees pertaining to the loan.’

Indeed, it is embedded in the pricing information from this market, which often forms they basis of comparison in valuing a subject interest.” (P. ” The International Valuation Glossary – Business Valuation (“the Glossary”) provides definitions of liquidity and marketability and their related discounts.

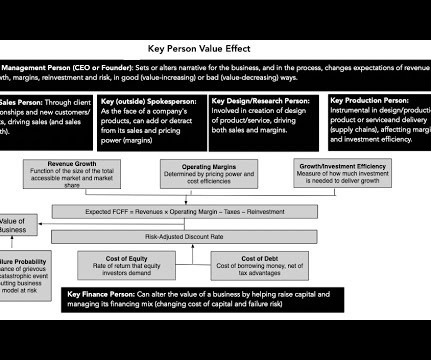

Key Person(s): Pricing effects It is true that markets are pricing mechanisms, not instruments for reflecting value, at least in the short term, and it should come as no surprise then that the effects of a key person are captured in pricing premiums or discounts, sometime arbitrary, and sometimes based upon data.

Were also bigger and had higher marketcapitalizations and better operating performance, on average. The expectation of larger future dividends relative to smaller future dividends would mitigate the marketability discount for the higher dividend-paying investment. This is just common sense. Refer to the initial figure.

No matter how you slice it, there is no denying that 2022 was the worst year for US equity investors since 2008, and the magnitude of the damage is even more staggering, if you consider it in market value terms. trillion in marketcapitalization, but for balance, it is also worth noting that US equities are still holding on to a gain of $6.9

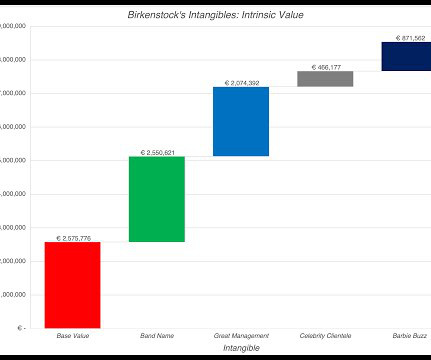

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies. Since Birkenstock generated revenues of $1.4

Further to our prior post about Delaware’s two new appraisal decisions, SWS Group was a small, struggling bank holding company that merged on January 1, 2015 into one of its own substantial creditors, Hilltop Holdings. Stockholders of SWS received a mix of cash and Hilltop stock worth $6.92 at closing. below the merger price.

The value of the stock is determined by an independent appraiser and is used to calculate the value of an employee's benefit under the plan. It's important to note that ESOP valuation is a complex process that should be conducted by a qualified appraiser with experience in ESOPs.

The value of the stock is determined by an independent appraiser and is used to calculate the value of an employee's benefit under the plan. It's important to note that ESOP valuation is a complex process that should be conducted by a qualified appraiser with experience in ESOPs.

The marketcapitalization of some small-cap stocks was 25 percent higher as a result of retail trading. Securities class actions depend on the fraud-on-the-market theory that assumes that stocks trade in an efficient market where public information about an issuer affects its stock price.

Since I am lucky enough to have access to databases that carry data on all publicly traded stocks, I choose all publicly traded companies, with a market price that exceeds zero, as my universe, for computing all statistics. Having toyed with alternative approaches, the one that I find offers the best balance is the aggregated ratio.

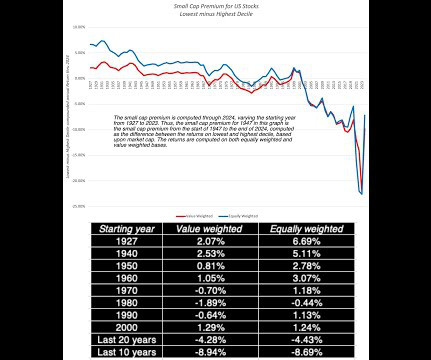

I follow up by looking at companies broken down by marketcapitalization, with an eye on whether the much-vaunted small cap premium has made a comeback. In the process, I also look how much the market owes its winnings to its biggest companies, with the Mag Seven coming under the microscope. Where does that leave us?

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content