This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

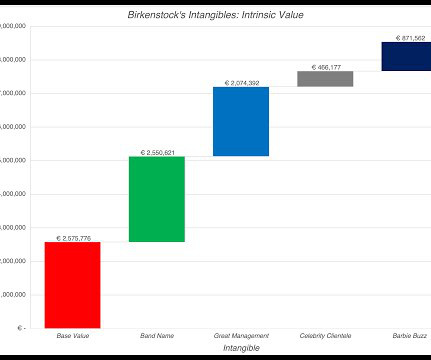

The Value of IntangibleAssets Accounting has historically done a poor job dealing with intangibleassets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent.

Business owners likely have particular ideas about the value of their company and how best to calculate it, given their experience and knowledge of their financial history, and understanding of the market and industry in which they operate. Asset Approach. Market Approach. >The

A common method under the asset approach is The Adjusted BookValue Method. This asset approach involves adjusting the bookvalue of a company’s assets and liabilities to reflect their current market values. The balance sheet lists the bookvalues of the company’s assets and liabilities.

If you're looking to deepen your understanding of business appraisal standards, this article dives into the significance of Revenue Ruling 59-60 and USPAP. Discover how these key guidelines help appraisers achieve accurate, fair, and legally defensible valuations. H2: How does USPAP affect business appraisal?

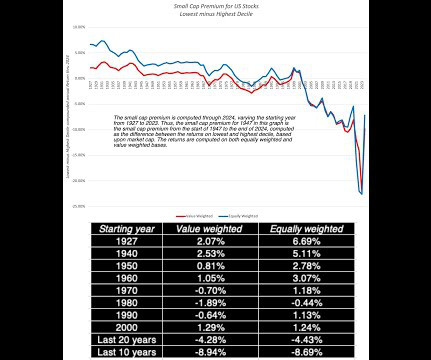

In my view, the small cap premium is not coming back, and given that it has been invisible for five decades now, the only explanation for why appraisers and analysts hold on to it is inertia. Momentum : In markets, the returns to value investing has generally moved inversely with the strength of momentum.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content