This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To capture the market's mood, I back out the expected return (and equity riskpremium) that investors are pricing in, through an implied equity riskpremium: Put simply, the expected return is an internal rate of return derived from the pricing of stocks, and the expected cash flows from holding them, and is akin to a yield to maturity on bonds.

Price of Risk The drop in stock and bond prices in the third quarter of 2023 can partly be attributed to rising interest rates, but how much of that drop is due to the price of risk changing? below the actual index level of 4288, making it close to fairly valued. below the index value of 4288, confirming my base case conclusion.

Exacerbating the pain, corporate default spreads rose during the course of 2022: While default spreads rose across ratings classes, the rise was much more pronounced for the lowest ratings classes, part of a bigger story about risk capital that spilled across markets and asset classes.

It is entirely possible that there will be a recession in 2024 or even in 2025, but what good is a signal that is two or three years ahead of what it is signaling? At the same time, not only has a recession not made its presence felt, but the economy showed signs of strengthening towards the end of the year.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. Beta & Risk 1. Equity RiskPremiums 2. Corporate Governance & Descriptive 1.

Posted by Arthur Korteweg (USC), Stavros Panageas (UCLA), and Anand Systla (UCLA), on Monday, February 3, 2025 Editor's Note: Arthur Korteweg is an Associate Professor of Finance and Business Economics at USC Marshall School of Business, Stavros Panageas is a Professor of Finance at UCLA Anderson School of Management, and Anand Systla is a Ph.D.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

Entering 2025, the gap between intrinsic and treasury rates has narrowed , as the market consensus settles in on expectations that inflation will stay about the Fed-targeted 2% and that economic activity will be boosted by tax cuts and a business-friendly administration. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks!

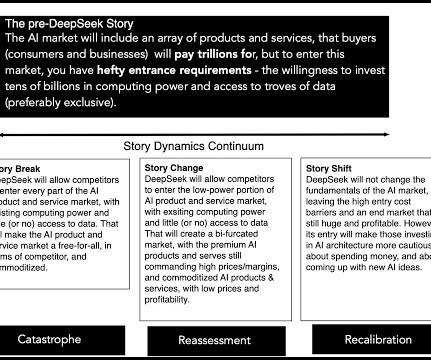

I graph the performance of the five AI stocks highlighted in the earlier section, throwing in the Meta and Microsoft for good measure, on a daily basis in 2025. YouTube Video Nvidia Valuations Nvidia valuation in September 2024 (Pre DeepSeek) Nvidia valuation in January 2025 (Post DeepSeek)

The February 18, 2025, Executive Order (Ensuring Accountability For All Agencies) threatens this balance. NYU Business School Professor Damoradans widely used valuation data, for example, currently shows the United States as having among the lowest equity riskpremiums in the world. [3]

17] See [link] (showing the United States has among the lowest equity riskpremiums in the world); Luzi Hail and Christian Leuz, International Differences in the Cost of Equity Capital: Do Legal Institutions and Securities Regulation Matter?, 11, 2025). [20] 12, 2025). [21] 12, 2025). [22] 12, 2025). [22]

With state and local taxes added on, the US, at the start of 2025, had a marginal corporate tax rate of 25%, almost perfectly in line with a global norm. The default spread is a price of risk in the bond market, and if you recall, I estimated the price of risk in equity markets, with an implied equity riskpremium, in my second data update.

The logical step in looking across countries is measuring risk in countries, and bringing that risk into your analysis, by incorporating that risk by demanding higher expected returns in riskier countries. The answers, to you, may seem obvious, but I find it useful to organize the obvious into buckets for analysis.

We’ve seen dramatic improvements with companies addressing maturities due in 2025, but also a lot of progress on maturities due out to 2026. The risk looks a lot better, and all those reasons support the soft-landing thesis. There are certain sectors that we think are offering better risk/reward.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. In the table below, I show my estimates of the implied equity riskpremium for the S&P 500 at the start of every month, since January 2024, and on March 14, 2025.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content