This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

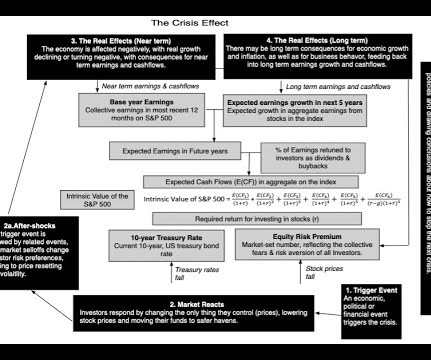

To capture the market's mood, I back out the expected return (and equity riskpremium) that investors are pricing in, through an implied equity riskpremium: Put simply, the expected return is an internal rate of return derived from the pricing of stocks, and the expected cash flows from holding them, and is akin to a yield to maturity on bonds.

Exacerbating the pain, corporate default spreads rose during the course of 2022: While default spreads rose across ratings classes, the rise was much more pronounced for the lowest ratings classes, part of a bigger story about risk capital that spilled across markets and asset classes.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. In the table below, we compare the changes in regional market capitalizations (in $ millions) over time.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

trillion in value last week, a 9.24% decline in value from the Friday close on March 28, 2025. There was undoubtedly some panic selling on Friday, but the flight to safety, whether it be in moving into treasuries or high dividend paying stocks, was muted. US equities had the biggest decline in dollar value terms, losing $5.3

Equity is cheaper than debt: There are businesspeople (including some CFOs) who argue that debt is cheaper than equity, basing that conclusion on a comparison of the explicit costs associated with each interest payments on debt and dividends on equity. YouTube Video Data Updates for 2025 Data Update 1 for 2025: The Draw (and Danger) of Data!

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. In the table below, I show my estimates of the implied equity riskpremium for the S&P 500 at the start of every month, since January 2024, and on March 14, 2025.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content