This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

That recovery notwithstanding, uncertainties about inflation and the economy remained unresolved, and those uncertainties became part of the market story in the third quarter of 2023. The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023.

That positive result notwithstanding, the recovery was uneven, with a big chunk of the increase in market capitalization coming from seven companies (Facebook, Amazon, Apple, Microsoft, Alphabet, NVidia and Tesla) and wide divergences in performance across stocks, in performance. increase in market capitalization.

Thus, looking at only the companies in the S&P 500 may give you more reliable data, with fewer missing observations, but your results will reflect what large market cap companies in any sector or industry do, rather than what is typical for that industry.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

As we start 2024, the interest rate prognosticators who misread the bond markets so badly in 2023 are back to making their 2024 forecasts, and they show no evidence of having learned any lessons from the last year. In fact, treasury bill rates consistently rise ahead of the Fed's actions over the two years.

See below for the latest set of upgrades and watch this space in early 2024 for more to come soon. New Professional Report Style: What? New Emerging Market Data (From EMIS): What? Stay tuned for more exciting and significant updates coming in early 2024. Available in Transactions Search. Why Important? Why Important?

Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). The rate would be calculated based on a 10-year "risk-free interest" rate depending on the currency, increased by a 1% riskpremium (1.5%

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equity riskpremiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time. It was the reason that I argued at a $1.2

Insurance industry terminology such as risk, premium, loss, deductibles, coverage limits, and perils are some of the fundamental concepts appraisers must grasp. Register for ASA’s PP163 Property Insurance Fundamentals: What Appraisers Need to Know webinar on June 6, 2024 from 2:00-3:00 PM EDT, presented by Thomas Dawson, ASA.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

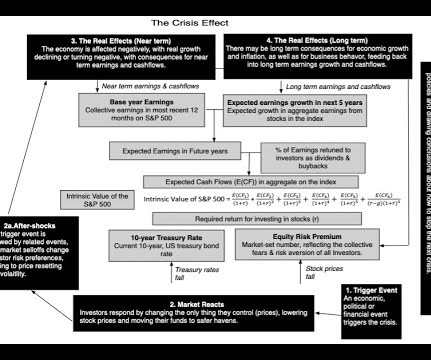

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

Coming after a few days where the market seemed to have found its bearings (at least partially), it was clear from the initial reactions across the world that the breadth and the magnitude of the tariffs had caught most by surprise, and that a market markdown was coming.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Equity RiskPremiums 2. Buybacks 2.

A little over a year later, in September 2024, that question about AI seemed to have been answered in the affirmative, for most investors, and I posted again after Nvidia had a disappointing earnings report , arguing that it reflected a healthy scaling down of expectations.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

With the peso stabilized, inflation reached 117% in December 2024, down from 292% from the years high in April, and the use of the dollar is expected to increase, including for day-to-day transactions. This may allow the country to reduce the riskpremium attached to its international borrowing. However, there are pros and cons.

The 40 Acts Prior to the 1929 stock market crash, a budding asset management industry was taking shape smaller investors were invited to pool their assets with the assets of others, mostly in closed-end funds. [3] 17] Markets are built on trust. Then Ill turn to some observations about the state of affairs as I see them today.

Effective and well-designed laws governing investment and financial markets are the single most important foundation for financial markets to allocate capital efficiently while providing optimal reassurance to investors and lenders. capital markets depends upon the regulatory certainty that U.S.

In this post, I will expand my analysis of data in 2024, which has a been mostly US-centric in the first four of my posts, and use that data to take you on my version of the Disney ride, but on this trip, I have no choice but to face the world as is, with all of the chaos it includes, with tariffs and trade wars looming.

Corporate control : There are companies that choose to borrow money, even though debt may not be the right choice for them, because the inside investors in these companies (family groups, founders) do not want to raise fresh equity from the market, concerned that the new shares issued will reduce their power to control the firm.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. Many of these hiring firms have supply chains that stretch across the world and sell their products and services in foreign markets.

Global Finance: What surprised you in 2024? Data has been better than we expected, not only in the labor market but also consumer spending remains very resilient. The market still expects that the Fed will be able to continue rate cuts at a regular cadence into next year. That’s a level we haven’t seen since 2005.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content