This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. Stocks: The What?

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Breaking equities down by sub-region, and looking across the globe, I computed the change in aggregate market capitalization, by region: While US stocks accounted for about $9.5

I looked at global equities, broken down by region of the world, and in US dollars, to allow for direct comparison: India is the only region of the world to post positive returns, in US dollar terms, in the third quarter, and is the best performing market of the year, running just ahead of the US; note again that of the $5.2

In my last three posts, I looked at the macro (equityriskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Cost of Equity 1.

DEBRA Proposal (« Debt-Equity Bias Reduction Allowance). In early May, the European Commission unveiled its proposal for a "DEBRA" (Debt-equity bias reduction allowance) Directive, aimed at encouraging companies to finance their investments with equity and capital contributions, instead of resorting to loans (bank or other).

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equityriskpremiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

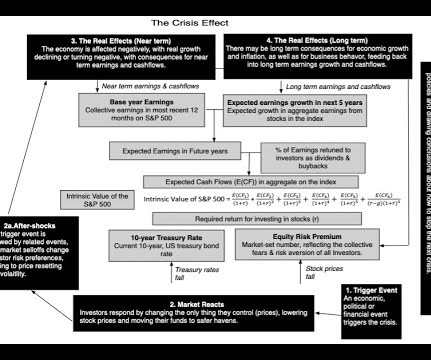

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equityriskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

Not surprisingly, the markets opened down on Thursday and spent the next two days in that mode, with US equity indices declining almost 10% by close of trading on Friday. US equities had the biggest decline in dollar value terms, losing $5.3

Thus, as you peruse my historical data on implied equityriskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed. In this post, I will begin by looking at movements in treasury rates, across maturities, during 2024, and the resultant shifts in yield curves.

A little over a year later, in September 2024, that question about AI seemed to have been answered in the affirmative, for most investors, and I posted again after Nvidia had a disappointing earnings report , arguing that it reflected a healthy scaling down of expectations.

14] Investment Company Institute, 2024 Investment Company Fact Book , at 22-23. [15] 17] See [link] (showing the United States has among the lowest equityriskpremiums in the world); Luzi Hail and Christian Leuz, International Differences in the Cost of Equity Capital: Do Legal Institutions and Securities Regulation Matter?,

Strong empirical evidence shows the United States has a lower cost of equity capital than comparable countries and that this lower cost is attributable in part to an institutional design that protects the independence of securities regulators and assures strong enforcement. In the United States, the cost of capital is lower than elsewhere.

The Debt Trade off As a prelude to examining the debt and equity tradeoff, it is best to first nail down what distinguishes the two sources of capital. To me, the key distinction between debt and equity lies in the nature of the claims that its holders have on cash flows from the business.

In this post, I will expand my analysis of data in 2024, which has a been mostly US-centric in the first four of my posts, and use that data to take you on my version of the Disney ride, but on this trip, I have no choice but to face the world as is, with all of the chaos it includes, with tariffs and trade wars looming.

Thus, my estimates of equityriskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. Not only does the world tilt more authoritarian than democratic in 2024, the trend line indicates that the world is becoming less democratic over time.

Global Finance: What surprised you in 2024? There are certain sectors that we think are offering better risk/reward. So, credit spreads have gotten so tight and so compressed that there’s not much of a cyclical riskpremium. GF: How does it look for private equity firms? That’s a level we haven’t seen since 2005.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content