This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

I am not a market prognosticator for a simple reason. I am just not good at it, and the first six months of 2023 illustrate why market timing is often the impossible dream, something that every investor aspires to be successful at, but very few succeed on a consistent basis.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

As we enter the last quarter of 2023, it has been a roller coaster of a year. In the first half of the year, we had positive surprises on both fronts, as inflation dropped after than expected and the economy stayed resilient, allowing for a comeback on stocks, which I wrote about in a post in July 2023.

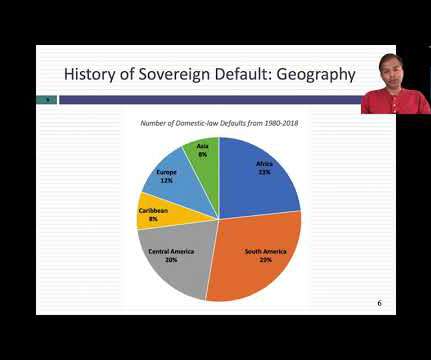

A few weeks ago, I posted my first data update pulling together what I had learned from looking at the data in 2023, and promised many more on the topic. Default Risk As with individuals and businesses, governments (sovereigns) borrow money and sometimes struggle to pay them back, leading to to the specter of sovereign default.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors. in 2022, higher than the 1- 1.5%

We also investigate whether litigation conveys valuable information to the market and how the competitive landscape changes both for indicted firms and their direct competitors. Our paper contributes to the discussion by examining fraud allegations, thus not restricting our investigation based on the eventual case outcome.

If equity markets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equity markets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

The other is pragmatic , since it is almost impossible to value a company or business, without a clear sense of how risk exposure varies across the world, since for many companies, either the inputs to or their production processes are in foreign markets or the output is outside domestic markets.

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. In that post, I noted that if inflation subsided quickly, and the economy stayed out of a recession, stocks had upside, and that is the scenario that played out in 2023.

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact.

My last valuation of Tesla was in November 2021, towards its market peak, and given its steep fall from grace, in conjunction with Elon Musk's Twitter experiment, it is time for a revisit.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery.

Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equity riskpremiums , I described the equity riskpremium as the additional return you would demand, over and above the risk free rate.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings!

Thus, looking at only the companies in the S&P 500 may give you more reliable data, with fewer missing observations, but your results will reflect what large market cap companies in any sector or industry do, rather than what is typical for that industry.

billion in gross profit in the last twelve months leading into 2023, but operating income drops off to $6.4 Finally, I look at the aggregated values across all companies on all three income measures, across all global companies, again broken down by sector: Collectively, global companies reported $16.9 billion and need income is only $4.3

In this post, I will focus on corporate debt in 2023, keeping in mind that it was a year where the tradeoffs changed, as interest rates rose to pre-2008 levels, and putting at risk those firms that had borrowed to capacity, or even beyond, at low interest rates.

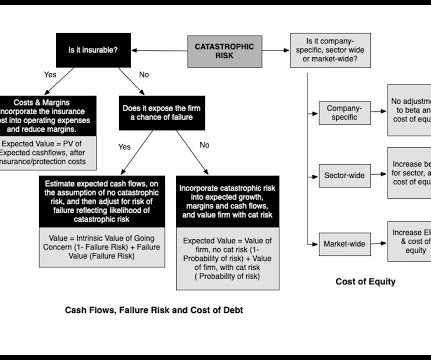

Deconstructing Risk While we may use statistical measures like volatility or correlation to measure risk in practice, risk is not a statistical abstraction. Its impact is not just financial, but emotional and physical, and it predates markets. 4 & 5 Uninsurable Risk.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equity riskpremiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time. and 10.9%. It was the reason that I argued at a $1.2

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). The rate would be calculated based on a 10-year "risk-free interest" rate depending on the currency, increased by a 1% riskpremium (1.5%

He is the Director of the Pepperdine Private Capital Markets Project (privatecap.org) and Executive Director for the Pepperdine Most Fundable Companies competition (pepperdine.edu/mfc). His teaching and research interests include entrepreneurial finance, private capital markets, and entertainment finance. Dr. Everett He holds a Ph.D.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Equity RiskPremiums 2. Buybacks 2.

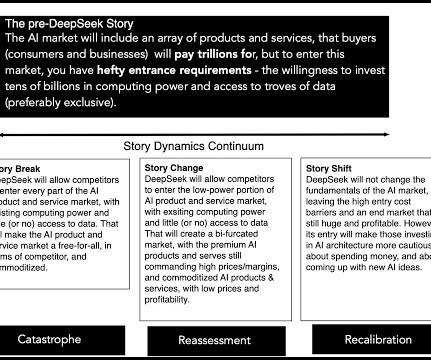

I first posted about AI in the context of valuing Nvidia , in June 2023, when there was still uncertainty about whether AI had legs. As the number of potential applications of AI proliferated, thus increasing the market for AI products and services, another part of the story was also being put into play.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. In 2022, the rise in rates was almost entirely driven by rising inflation expectations , with the Fed racing to keep up with that market sentiment.

The main attraction of full dollarization is the elimination of the risk of a sudden, sharp devaluation of the countrys exchange rate, the IMF writers point out. This may allow the country to reduce the riskpremium attached to its international borrowing. in 2023, according to World Bank data. by 2006 and was 24.1%

The Indian and Chinese markets cooled off in 2024, posting single digit gains in price appreciation. The Indian and Chinese markets cooled off in 2024, posting single digit gains in price appreciation. I converted all of the market capitalizations into US dollars , just to make them comparable.

Corporate control : There are companies that choose to borrow money, even though debt may not be the right choice for them, because the inside investors in these companies (family groups, founders) do not want to raise fresh equity from the market, concerned that the new shares issued will reduce their power to control the firm.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. Many of these hiring firms have supply chains that stretch across the world and sell their products and services in foreign markets.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content