This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I am just not good at it, and the first six months of 2023 illustrate why market timing is often the impossible dream, something that every investor aspires to be successful at, but very few succeed on a consistent basis. Markets, as is their wont, live to surprise, and the first six months of 2023 has wrong-footed the experts (again).

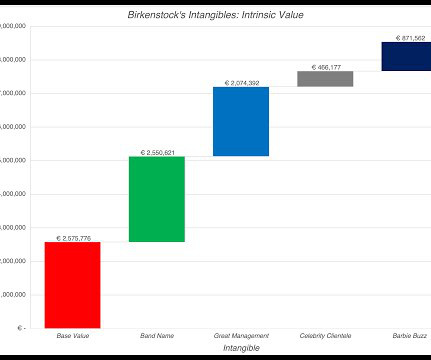

In this post, I will look at another initial public offering, Birkenstock, that is likely to get more attention in the next few weeks, given that it is targeting to go public at a pricing of about €8 billion, for its equity, in a few weeks. So, how far has accounting come in bringing intangible assets on to balance sheets?

Finally, I look at the aggregated values across all companies on all three income measures, across all global companies, again broken down by sector: Collectively, global companies reported $16.9 billion in gross profit in the last twelve months leading into 2023, but operating income drops off to $6.4

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital. trillion ($1.8

Return on Equity 1. Equity Risk Premiums 2. Costs of equity & capital 4. Costs of equity & capital 1. Fundamental Growth in Equity Earnings 2. Return on Equity 2. Standard Deviation in Equity/Firm Value 2. BookValue Multiples 3. Beta & Risk 1. Debt Details 1.

06, 2023 (GLOBE NEWSWIRE) -- Equity Bancshares, Inc. NYSE: EQBK ) ("Equity" or the "Company"), the Wichita-based holding company of Equity Bank, announced today its entry into a definitive merger agreement with Rockhold Bancorp ("Rockhold"), the parent company of the Bank of Kirksville in Kirksville, Missouri.

For example, I have seen it asserted that a stock that trades at less than bookvalue is cheap or that a stock that trades at more than twenty times EBITDA is expensive. In January 2023, I ended up with 47,913 publicly traded firms in my sample , with the pie chart below providing a geographic breakdown. Cost of Equity 1.

stake in Wella for $150 million, reflecting a 4% premium to the bookvalue of Wella as of March 31, 2023. Coty Inc (NYSE: COTY ) has entered into a binding letter of intent to sell a portion of its Wella beauty and hair care brand stake to investment firm IGF Wealth Management. Coty will sell a 3.6%

and 0.91%, Respectively, Excluding Non-Recurring Expenses First Quarter 2023 Loan Growth of $22.1 Non-performing Assets were 0.14% of Total Assets at March 31, 2023 Common Equity Tier 1 and Tangible Common Equity Ratio of 12.16% and 7.63%, Respectively, at March 31, 2023 1 LAKEVILLE, Conn., million, or 1.8%

July 25, 2023 (GLOBE NEWSWIRE) -- Banc of California, Inc. July 25, 2023 (GLOBE NEWSWIRE) -- Banc of California, Inc. Financial Benefits of the Merger The financial benefits of the transaction are compelling, with estimated 2024 EPS and tangible bookvalue accretion of 20+% and ~3%, respectively. and BEVERLY HILLS, Calif.,

April 28, 2023 (GLOBE NEWSWIRE) -- Mid Penn Bancorp, Inc. NASDAQ: MPB ) ("Mid Penn"), the parent company of Mid Penn Bank (the "Bank") and MPB Financial Services, LLC, today reported net income available to common shareholders ("earnings") for the quarter ended March 31, 2023 of $11.2 HARRISBURG, Pa.,

“Wind farms are valued at €0.8m – €1.2m SaaS start-ups are valued at 10x Sales”. Equity Vs. Enterprise Multiples – Which To Use? The ratio is either related to the EquityValue or ratios related to the Enterprise Value. . An example of an equity multiple: Price / Earnings.

“Wind farms are valued at €0.8m – €1.2m SaaS start-ups are valued at 10x Sales”. Equity Vs. Enterprise Multiples – Which To Use? The ratio is either related to the EquityValue or ratios related to the Enterprise Value. . An example of an equity multiple: Price / Earnings.

Based on S&P Capital IQ Pro data as of June 30, 2023, First of Long Island is ranked #4 in Nassau County and #5 in Suffolk County in deposit market share among banks under $100 billion of assets. "We Tangible bookvalue per share dilution is projected at 12%, with an earnback period of approximately 2.9 billion of deposits.

March 21, 2023 (GLOBE NEWSWIRE) -- First Mid Bancshares, Inc. Based on First Mid's price per share at closing on March 20, 2023 of $27.13, the aggregate consideration to be paid by First Mid is approximately $90.3 Estimated tangible bookvalue per share dilution to First Mid is expected to be earned back in 1.9

billion – − Highly synergistic platforms and capital optimization will drive strong earnings per share accretion in 2024 and sustained long-term growth − − Expected value at closing of approximately $787 million − NEW YORK, Feb. Upon completion of the merger, Ready Capital is expected to have a pro forma equity capital base of $2.8

At or immediately prior to the closing, IFH is expected to distribute its minority equity interest in Dogwood State Bank to IFH shareholders in the form of a dividend equal to approximately 0.469 shares of Dogwood State Bank for each share of IFH common stock, a value of $7.69/share and Capital Bank. and Capital Bank.

per basic and diluted share, for the three months ended June 30, 2023. per basic and diluted share, for the six months ended June 30, 2023. million for the respective 2023 periods. and 16.7%, respectively, versus the same period in 2023. per basic and diluted share, for the three months ended June 30, 2023.

According to researcher Giuliano Bologna at Compass Point Research and Trading , Inc: In the third quarter of 2023, only six us banks had non-mortgage consumer loans (personal, student, etc), measured at fair value, with SoFi’s loans making up more than 95% of the total. and its CET1 ratio would be cut from 14.3 percent to 8.9

million in tangible common equity. accretive to estimated 2023 and 2024 diluted earnings per share, respectively. Tangible bookvalue per share will be diluted approximately (2.1%) at closing and is expected to be recovered in 3.25 At March 31, 2022, PPSF reported $132.7 million in total assets, $99.9

Credit Suisse (CS) was sold to UBS on March 19, 2023, to avoid its further deterioration from long-lasting distress and widespread distrust, especially after the collapse of Silicon Valley Bank. According to the 2022 CS Annual Report , the bookvalue per share was 11.45 Swiss francs (CHF) per share. percent per year).

06, 2023 (GLOBE NEWSWIRE) -- Intact Financial Corporation (TSX: IFC ) (Intact, IFC or the Company) and its subsidiary RSA today announced that they have reached an agreement with Direct Line Insurance Group plc (Direct Line) to acquire Direct Line's brokered Commercial Lines operations.

HOUSTON, Texas, July 10, 2023 (GLOBE NEWSWIRE) -- via NewMediaWire -- SMG Industries Inc. With the completion of this transaction, SMGI's balance sheet is significantly improved, including a large increase in the bookvalue of the combined company.

they opted for pooling accounting, in which goodwill was not recognized and therefore not amortized; the bookvalue of the assets and liabilities of the two businesses were just added together. This derives from value-relevance being the main accounting objective in the U.S., Initially they favored hiding goodwill. In the U.S.

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporate finance. To illustrate the heat that buybacks evoke, consider two stories in the last two weeks where they have been in the news.

In this post, I will begin by looking at how to value banks and follow up with an examination of investor views of banking have changed, by looking at pricing, before examining divergences in how banks are priced in the market today. All Equity, All the time!

In this post, I will focus on corporate debt in 2023, keeping in mind that it was a year where the tradeoffs changed, as interest rates rose to pre-2008 levels, and putting at risk those firms that had borrowed to capacity, or even beyond, at low interest rates.

Higher interest rates have given banks some relief over the past few years, increasing their net interest income while hampering competitors—particularly fintech startups dependent on equity financing. Equity investors value Visa at 29 times earnings and 13 times bookvalue, according to Bloomberg.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like market capitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

Thus, as you peruse my historical data on implied equity risk premiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In my first two data posts for 2025, I looked at the strong year that US equities had in 2024, but a very good year for the overall market does not always translate into equivalent returns across segments of the market. In this post, I will remain focused on US equities, but I will break them into groupings, looking for differences.

The Debt Trade off As a prelude to examining the debt and equity tradeoff, it is best to first nail down what distinguishes the two sources of capital. To me, the key distinction between debt and equity lies in the nature of the claims that its holders have on cash flows from the business.

I aggregated the market capitalizations of all stocks at the end of 2023 and the end of 2024, and computed the percentage change. The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content