This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

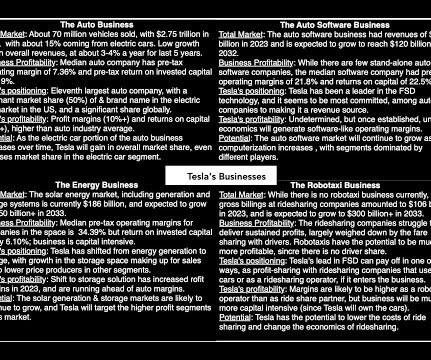

As the price dropped below $200 today (October 30,2023), I decided that it was time for me to revisit and revalue the company, taking into account the news, financial and other, that has come out since my last valuation in January 2023, and to understand the dueling stories that are emerging about the company.

Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world. In January 2023, I ended up with 47,913 publicly traded firms in my sample , with the pie chart below providing a geographic breakdown. Cost of Capital 3. Cost of Equity 1.

Since I am lucky enough to have access to databases that carry data on all publicly traded stocks, I choose all publicly traded companies, with a market price that exceeds zero, as my universe, for computing all statistics. Beta & Risk 1. Return on (invested) capital 2. Return on Equity 1. Debt Ratios & Fundamentals 1.

In this post, I will focus on corporate debt in 2023, keeping in mind that it was a year where the tradeoffs changed, as interest rates rose to pre-2008 levels, and putting at risk those firms that had borrowed to capacity, or even beyond, at low interest rates.

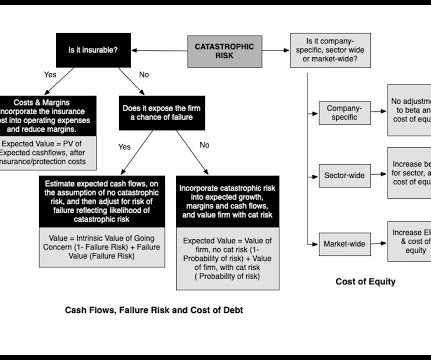

Intrinsic Value Effect : The calculations for cashflows are identical to those done when the risks are company-specific, with cash flows estimated with and without the catastrophic risk, but since these risks are sector-wide or market-wide, there will also be an effect on discount rates. at the end of 2007 to 0.85 two years later.

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content