This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

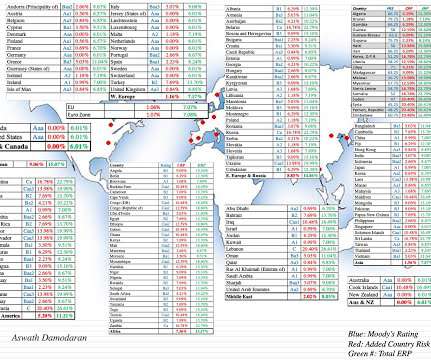

Country Risk: Default Risk and Ratings For investors, the most direct measures of country risk come from measures of their capacity to default on their borrowings. Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries.

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact. in the NY Fed survey.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

At close of trading on July 26, 2022, the stock was trading at ? In this post, I will begin with a quick review of my 2021 valuation, then move on to the price action in 2021 and 2022 and then update my valuation to reflect the company's current numbers. 46 in July 2022. 68746 (including short term investments) in March 2022.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term. at the start of that year.

Happy New Year, and I hope that 2022 brings you good tidings! In short, and at the risk of stating the obvious, having access to data is a benefit but it is not a panacea to every problem. Sometimes, less is more! It is also why I report only aggregated data on industries, rather than company-level data.

It is precisely because we have been spoiled by a decade of low and stable inflation that the inflation numbers in 2021 and 2022 came as such a surprise to economists, investors and even the Fed.

In this section, I will begin measures of country default risk, including sovereign ratings and CDS spreads, before moving to more expansive measures of country risk before concluding with measures of equity riskpremiums for countries, a pre-requisite for estimating the values of companies with operations in those countries.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. That pessimism was not restricted to market outlooks.

In 2022, as bond rates have risen, stock prices have fallen, and crypto has imploded, even true believers are questioning what the bottom for markets might be, and when we will get there. That pullback has had its consequences, with equity riskpremiums rising around the world.

While stocks had their ups and downs during the year, they ended the year strong, and recouped, at least in the aggregate, most of the losses from 2022. Energy, one of the few survivors of the 2022 market sell-off, had a bad year, as did utilities and consumer staples. The solid comeback in stocks, though, came with caveats.

We started the year with significant uncertainty about whether the surge in inflation seen in 2022 would persist as well as about whether the economy was headed into a recession. The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. That is good advice in most years, but 2022 was not one of those years. Since inflation was 6.42% in 2022, the real return on a US 10-year treasury bond was -22.79%.

Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums. It is true that economists have researched risk aversion for centuries and concluded that investors are collectively risk averse, and that the level of risk aversion varies across age groups, income levels and time.

With this investment, you face price risk , since even though you know what you will receive as a coupon or cash flow in future periods, since the present value of these cash flows, will change as rates change. For an investment to be risk free then, it has to meet two conditions. and the reverse will occur, when risk-free rates drop.

Note, though, that while sovereign CDS spreads increased almost 51% between January 1, 2022 and March 16, 2022, in these countries, the overall riskiness of the region remains low, the average spread at 1.30%.

Government Bond/Bill Rates in 2023 I will start by looking at government bond rates across the world, with the emphasis on US treasuries, which suffered their worst year in history in 2022, down close to 20% for the year, as interest rates surged. 4.50%, by the end of the year.

Beta & Risk 1. Equity RiskPremiums 2. I also have implied equity riskpremiums (forward-looking and dynamic estimate of what investors are pricing stocks to earn in the future) for the S&P 500 going back annually to 1960 and monthly to 2008, and equity riskpremiums for countries. Buybacks 2.

Tesla's rise is summarized in the graph below, where we look at the company's revenues and earnings over time, with earnings measured in gross and operating terms, and EBITDA capturing operating cash flows: 2022 numbers updated to reflect 4th quarter earnings call on 1/25/23 Between 2010 and 2020, Tesla grew revenues from $117 million to $31.5

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Debt breakdown 2.

By the end of 2021, it was clear that this bout of inflation was not as transient a phenomenon as some had made it out to be, and the big question leading in 2022, for investors and markets, is how inflation will play out during the year, and beyond, and the consequences for stocks, bonds and currencies.

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasury rates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

The definition of "net equity" is as follows: equity of the company = sum of subscribed capital, share premiums, revaluation reserves, reserves and retained earnings, minus the tax value of the company's holdings in associated companies and the tax value of its own shares. riskpremium if the company is an SME as defined by European law).

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equity riskpremiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time. and 10.9%.

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. But as I noted in my data post on interest rates, the last year (2022) has been a most unusual one, in terms of interest rate moves, in developed markets.

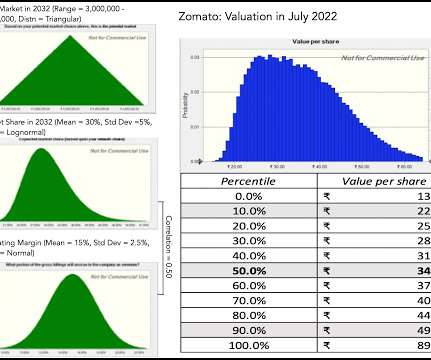

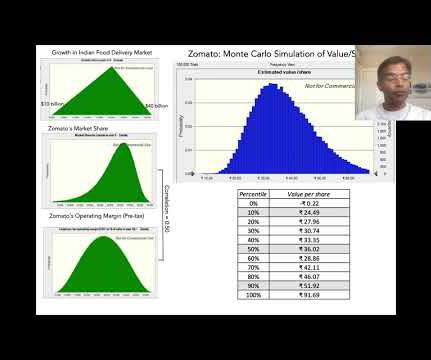

I will assume a partial bounce back to 22% of GOV , starting in 2022, but the presence of Amazon Food will prevent a return to higher values in the future. Revenue Share : While the market share and total market yield the gross order value for Zomato, the company posts only its share of these orders, as revenues.

He is a frequent presenter on valuation topics, and is currently a subject matter expert on the Appraisal Foundation’s working group preparing a Valuation Advisory on the Company-Specific RiskPremium. Michael is part of the industrial products industry group of the firm and co-head of U.S.

Risk Differences across Countries In this final section, I will look risk differences across countries, both in terms of why risk varies across, as well as how these variations play out as equity riskpremiums.

With stocks, I compute this pre-personal tax return at the start of every month, using the current level of index and expected cash flows to back out an internal rate of return; this is the basis for the implied equity riskpremium. It is one more reason that blindly using historical riskpremiums can lead to static and strange values.

In 2022, North America and Western Europe scored highest on the democracy index, and Middle East and Africa scored the lowest. For three decades, I have wrestled with measuring this additional risk exposure and converting that measurement into an equity riskpremium, but it remains a work in progress.

In the last week of February 2022, in the immediate aftermath of this crisis, there were a few ESG supporters who argued that ESG-based investors were less exposed to the damage from the crisis. billion invested in Russian equities on February 23, 2022 , almost all of which was wiped out during the next few weeks.

Computing the returns in real terms , by taking out inflation in each year from that year's returns, and recomputing the equity riskpremiums: Download historical data Note that the equity riskpremiums move only slightly, because inflation finds its way into both stock and treasury returns.

I will follow up by examining changes in corporate bond rates, across the default ratings spectrum, trying to get a measure of how the price of risk in bond markets changed during 2024. In 2022, the rise in rates was almost entirely driven by rising inflation expectations , with the Fed racing to keep up with that market sentiment.

That said, the AI story broke out to the public on November 30, 2022, when OpenAI launched ChatGPT, and it made its presence felt in homes, schools and businesses almost instantaneously. The other is that the stock is overvalued, at its current price of $123 per share, even after the markdown this week.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

The default spread is a price of risk in the bond market, and if you recall, I estimated the price of risk in equity markets, with an implied equity riskpremium, in my second data update. The first was whether companies would pull back from borrowing , with the higher rates, leading to a drop in aggregate debt.

That’s the tightest since 2022. There are certain sectors that we think are offering better risk/reward. So, credit spreads have gotten so tight and so compressed that there’s not much of a cyclical riskpremium. You’re not being rewarded as an investor for taking on that extra risk given how tight spreads have become.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content