This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

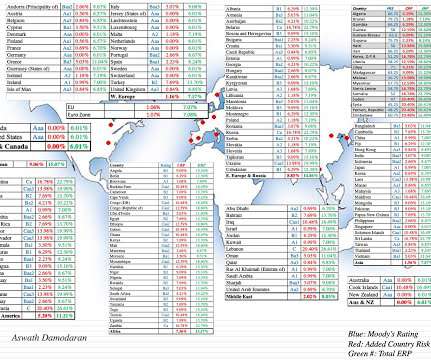

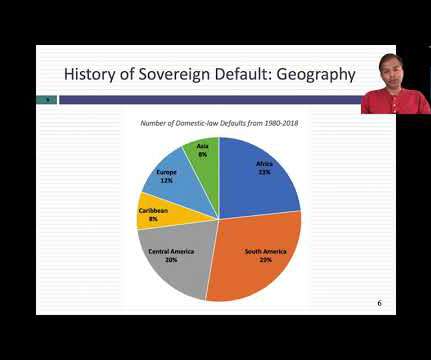

Country Risk: Default Risk and Ratings For investors, the most direct measures of country risk come from measures of their capacity to default on their borrowings. Third, corruption operates as an implicit tax , since business operating in corrupt parts of the world have to build in the associated costs and constraints.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term. Stocks: The What? at the start of that year.

If you have been reading my posts, you know that I have an obsession with equityrisk premiums, which I believe lie at the center of almost every substantive debate in markets and investing. How, you may ask, can equityrisk premiums be that divergent, and does that imply that anything goes?

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

By the end of 2021, it was clear that this bout of inflation was not as transient a phenomenon as some had made it out to be, and the big question leading in 2022, for investors and markets, is how inflation will play out during the year, and beyond, and the consequences for stocks, bonds and currencies.

We started the year with significant uncertainty about whether the surge in inflation seen in 2022 would persist as well as about whether the economy was headed into a recession. The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors.

It is precisely because we have been spoiled by a decade of low and stable inflation that the inflation numbers in 2021 and 2022 came as such a surprise to economists, investors and even the Fed.

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of risk premiums.

In the month since, I have added two more data updates, one on US equities and one on interest rates , but my attention was drawn away by other interesting stories. It is also the aspect of country risk, where there is the longest history of measurement, and there are widely used measurement tools.

Tesla's rise is summarized in the graph below, where we look at the company's revenues and earnings over time, with earnings measured in gross and operating terms, and EBITDA capturing operating cash flows: 2022 numbers updated to reflect 4th quarter earnings call on 1/25/23 Between 2010 and 2020, Tesla grew revenues from $117 million to $31.5

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery. In fact, treasury bill rates consistently rise ahead of the Fed's actions over the two years.

The second was the drop in the Fed Funds rate to close to zero percent, first after the 2008 crisis and then again after the COVID shock in the first quarter of 2020. While the Federal Open Market Committee controls the Fed Funds rate, there are a whole host of rates set by buyer and sellers in bond markets.

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasury rates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

Use of Special purpose acquisition (SPAC) vehicles have spiked over the past year because private equity and venture capital firms have excess cash they need to put to work, accounting practitioners said mid-June. These standards require companies to assess whether the warrants should be equity or liability classified.

The first of the is as companies scale up, there will be a point where they will hit a growth wall, and their growth will converge on the growth rate for the economy. In short, I am assuming that the price cuts and cost pressures of the fourth quarter are more representative of what Tesla will face in the future, as competition steps up.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

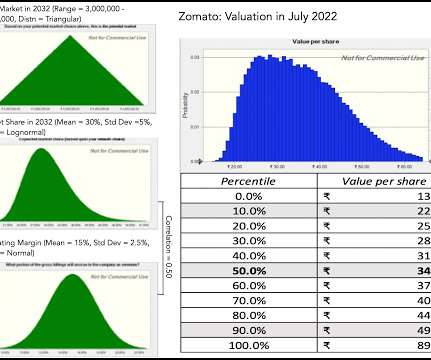

At close of trading on July 26, 2022, the stock was trading at ? In this post, I will begin with a quick review of my 2021 valuation, then move on to the price action in 2021 and 2022 and then update my valuation to reflect the company's current numbers. grow at the cost of equity), yielding about ?46 46 in July 2022.

Happy New Year, and I hope that 2022 brings you good tidings! In short, and at the risk of stating the obvious, having access to data is a benefit but it is not a panacea to every problem. Sometimes, less is more! It is also why I report only aggregated data on industries, rather than company-level data.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

In 2022, North America and Western Europe scored highest on the democracy index, and Middle East and Africa scored the lowest. For three decades, I have wrestled with measuring this additional risk exposure and converting that measurement into an equityrisk premium, but it remains a work in progress.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

I will follow up by examining changes in corporate bond rates, across the default ratings spectrum, trying to get a measure of how the price of risk in bond markets changed during 2024. Put simply, with or without the Fed, rates would have been low during the period.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content