This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Leading into 2021, the big questions facing investors were about how quickly economies would recover from COVID, with the assumption that the virus would fade during the year, and the pressures that the resulting growth would put on inflation.

Consequently, you can only value the equity in a bank, and by extension, the only pricing multiples you can use to price banks are equity multiples (PE, Price to Book etc.).

Inflation numbers have been coming in high now, for more than a year, but for much of the early part of 2021, bankers, investors and politicians seemed to be either in denial or casually dismissive of its potential for damage.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms. Data Update 2 for 2021: The Price of Risk!

It is true that economic activity has leveled off and housing prices have declined a little, relative to a year ago, but given the rise in rates in 2022, those changes are mild. If anything, the economy seems to have settled into a stable pattern, albeit at the high levels that it reached in the second half of 2021.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The Interest Rates Story To me the biggest story of markets in 2021 has been the rise of interest rates, especially at the long end of the maturity spectrum. for 2021 and inflation of 2.2%

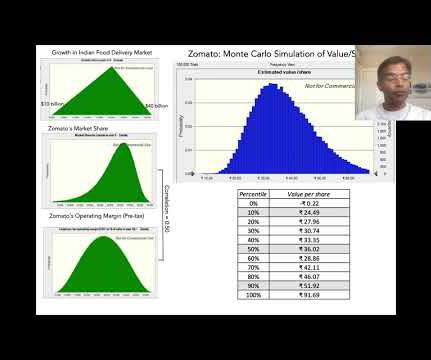

Zomato, an Indian online food-delivery company, was opened up to public market investors on July 14, 2021, and its market debut is being watched for clues by a number of other online ventures in India, waiting in the wings to go public. The service was initiated in 2017 and it had 1.5

In 2021, it sold more than 100,000 battery electric vehicles (BEV). The company missed its 2021 sales target by 4% amid the chip crisis. Book value is the value attributable to shareholders in case the company sells all its assets and repays its liabilities (also called liquidation value). Fuel cell electric vehicles (FCEV).

Russia was also a leading exporter of these commodities, with a disproportionately large share of its oil and gas production going to Europe; in 2021, Russian gas accounted to 45% of EU gas imports. Ukraine is also primarily a natural resource producer, especially iron ore, albeit on a smaller scale.

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. Source Data The two estimates move together much of the time, but the consumer expectations are consistently higher, and at the end of April 2021, the consumer survey was forecasting inflation of 3.2%, about 1.1%

I also report on pricing statistics, again broken down by industry grouping, with equity (PE, Price to Book, Price to Sales) and enterprise value (EV/EBIT, EV/EBITDA, EV/Sales, EV/Invested Capital) multiples. Standard deviation in stock price 2. Price to Book 3. High-Low Price Risk Measure 5.

The company's return on invested capital has steadily declined, even as it has scaled up, hovering just over 3% in 2021-2022. You see similar movements in the price to book, where the stock has gone from trading under book value to 6.7 times revenues in the most recent two years.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content