This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

2022 brought a halt to a nearly unabated 12-year run of booming credit markets and “lower for longer” interest rates. high-yield bond issuances were down approximately three quarters year-over-year – the lowest volume since 2008 – while newly minted leveraged loans fell nearly two-thirds from 2021 levels. over the same period.

Leading into 2021, the big questions facing investors were about how quickly economies would recover from COVID, with the assumption that the virus would fade during the year, and the pressures that the resulting growth would put on inflation. The year that was.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

Inflation numbers have been coming in high now, for more than a year, but for much of the early part of 2021, bankers, investors and politicians seemed to be either in denial or casually dismissive of its potential for damage. While the implied inflation in bond rates is low, investors seem to be anticipating higher inflation.

Investors are constantly in search of a single metric that will tell them whether a market is under or over valued, and consequently whether they should buying or selling holdings in that market. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of risk premiums.

Capital Constrained Clearing Rate : The notion that any investment that earns more than what other investments of equivalent risk are delivering is a good one, but it is built on the presumption that businesses have the capital to take all good investments.

lived under full democracy, in 2021, with large differences across regions. I know that there are some of you, who distrust ratings agencies, arguing that they have regional and other biases and/or that they do not adjust ratings in a timely fashion.

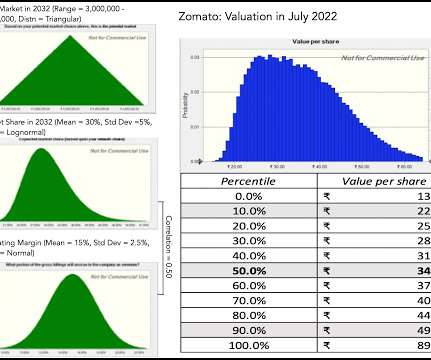

On July 21, 2021, I valued Zomato just ahead of its initial public offering at about ? The market clearly had a very different view, as the stock premiered at ? 169 per share in late 2021. per share, and the mood and momentum that worked in its favor for most of 2021 had turned against the company. 41 per share.

Convertible Arbitrage Definition: Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; the fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall marketrisk.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation.

I have been writing about, and valuing, Tesla for most of its lifetime in public markets, and while it remains a company that draws strong reactions, it is also one that I truly enjoy valuing. Tesla: The Back Story I first valued Tesla in 2013 , as a "luxury automobile company" and I have valued almost every year since.

My last valuation of Tesla was in November 2021, towards its market peak, and given its steep fall from grace, in conjunction with Elon Musk's Twitter experiment, it is time for a revisit. In this section, I will begin by looking at the evolution of my Tesla value from 2013 to 2021, and then present my updated valuation of the company.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. I was a believer in big data and crowd wisdom, well before those terms were even invented.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond marketrates, with a concurrent rise in default spreads exacerbating the damage to investors.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

The nature of markets is that they are never quite settled, as investors recalibrate expectations constantly and reset prices. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

Thus, looking at only the companies in the S&P 500 may give you more reliable data, with fewer missing observations, but your results will reflect what large market cap companies in any sector or industry do, rather than what is typical for that industry.

I think that the market is too pessimistic about the long-term outlook. As of 2021, Idemitsu has a cash-to-assets ratio of 3%. Historically, Japan has a very low risk-freerate. By 2030, the company plans to increase its renewable capacity to 4 Gigawatt from currently 0.2 Balance sheet – Idemitsu Kosan.

A few of you did take issue with the fact that the growth rate that I used for the first five years dropped from 35%, in my November 2021 valuation , to 24%, in my most recent one. Put simply, there are very, very few companies that generate big revenues and earn high margins at the same time. It was the reason that I argued at a $1.2

I take the point of view that uncertainty should not stop you from valuing companies, that your value estimates will have more error in them, but since the market also faces the same uncertainty, your best bargains may be in the midst of uncertainty. pm (New York time) All three classes start on February 1, 2021 and end on May 10, 2021.

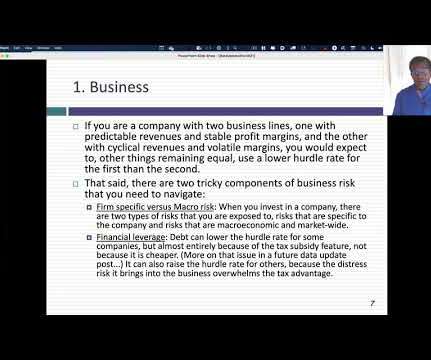

In my last three posts, I looked at the macro (equity risk premiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

The first is to see how the increase in inflation in 2021 and 2021 has played out in profitability for companies, since inflation can increase profits for some firms, and lower them for others. the returns you can make on investments of equivalent risk, and that game became a lot more difficult to win in 2022.

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. All of these measures, no matter how carefully designed, give a measure of inflation in the past, and markets are ultimately concerned more with inflation in the future. Louis estimates for inflation rates exceeding 2.5%

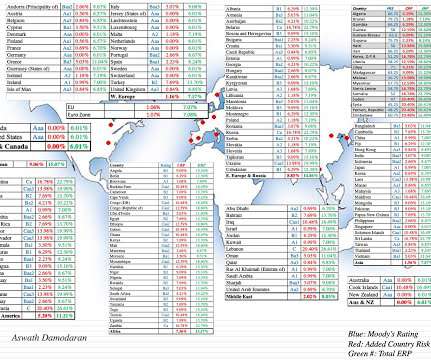

The other is pragmatic , since it is almost impossible to value a company or business, without a clear sense of how risk exposure varies across the world, since for many companies, either the inputs to or their production processes are in foreign markets or the output is outside domestic markets.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content