This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Leading into 2021, the big questions facing investors were about how quickly economies would recover from COVID, with the assumption that the virus would fade during the year, and the pressures that the resulting growth would put on inflation. The year that was.

In 2022, we needed that reminder more than ever before, especially after markets came roaring back from the COVID drop in 2020 and 2021. We invest in equities expecting to earn more than we can make on risk free or guaranteed investments, but the risk in equities is that actual returns can deviate from expectations.

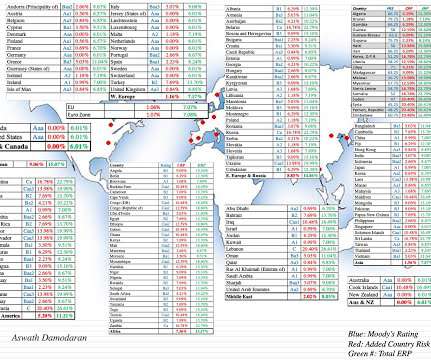

lived under full democracy, in 2021, with large differences across regions. Country Risk: EquityRisk For equity investors, the price of risk is captured by the equityriskpremium, and equityriskpremiums will vary across countries.

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums.

In my early 2021 posts on inflation, I argued that while the higher inflation that we were just starting to see could be explained by COVID and supply chain issues, prudence on the part of policy makers required that it be taken as a long term threat and dealt with quickly. in the NY Fed survey.

Cost of raising funds (capital) : Since the funds that are invested by a business come from equity investors and lenders, one way in which the hurdle rate is computed is by looking at how much it costs the investing company to raise those funds. US , Europe , Emerging Markets , Japan , Australia/NZ & Canada , Global ) 2.

And Consequences If you are wondering why you should care about risk capital's ebbs and flows, it is because you will feel its effects in almost everything you do in investing and business. While the number of IPOs in 2021 is still below the peak dot-com years, the proceeds from IPOs has surged to an all-time high during the year.

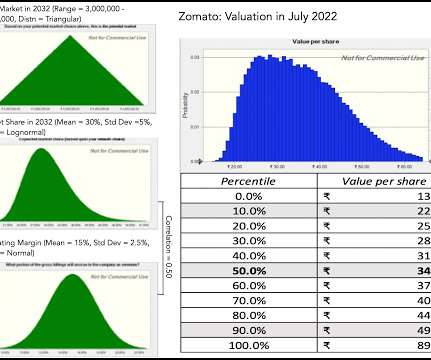

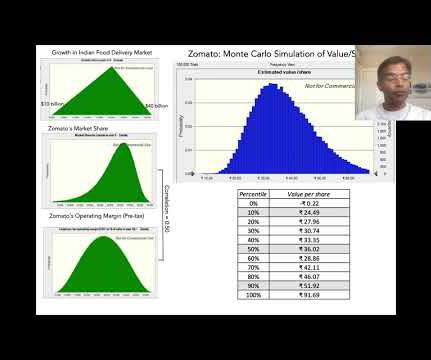

On July 21, 2021, I valued Zomato just ahead of its initial public offering at about ? 169 per share in late 2021. per share, and the mood and momentum that worked in its favor for most of 2021 had turned against the company. grow at the cost of equity), yielding about ?46 15,000 in March 2021 to ? 41 per share.

It is precisely because we have been spoiled by a decade of low and stable inflation that the inflation numbers in 2021 and 2022 came as such a surprise to economists, investors and even the Fed. As the inflation bogeyman returns, the worries of what may need to happen to the economy to bring inflation back under control have also mounted.

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Breaking equities down by sub-region, and looking across the globe, I computed the change in aggregate market capitalization, by region: While US stocks accounted for about $9.5

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. trillion below their values from the start of 2022. that was lost last year.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The Interest Rates Story To me the biggest story of markets in 2021 has been the rise of interest rates, especially at the long end of the maturity spectrum. for 2021 and inflation of 2.2%

Those measures took a beating in 2020, as COVID decimated the earnings of companies in many sectors and regions of the world, and while 2021 was a return to some degree of normalcy, there is still damage that has to be worked through.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equityriskpremiums , I described the equityriskpremium as the additional return you would demand, over and above the risk free rate.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. Historical Context In my earlier post, I noted that US equity market performance in 2022 made it the seventh worst year in stock market history, if you go back to 1928.

Inflation numbers have been coming in high now, for more than a year, but for much of the early part of 2021, bankers, investors and politicians seemed to be either in denial or casually dismissive of its potential for damage.

Russia was also a leading exporter of these commodities, with a disproportionately large share of its oil and gas production going to Europe; in 2021, Russian gas accounted to 45% of EU gas imports. As Russian equities have imploded, the ripple effects again are being felt across the globe.

In my last post , I described the wild ride that the price of risk took in 2020, with equityriskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

My last valuation of Tesla was in November 2021, towards its market peak, and given its steep fall from grace, in conjunction with Elon Musk's Twitter experiment, it is time for a revisit. In this section, I will begin by looking at the evolution of my Tesla value from 2013 to 2021, and then present my updated valuation of the company.

In 2021, looking at the company, I feel more convinced than I was a few years that it is, at its core, an automobile company, and while it will continue to derive revenues from batteries and perhaps even software, its pathway to becoming a trillion dollar market cap company still runs through the "car company" story.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Cost of Equity 1.

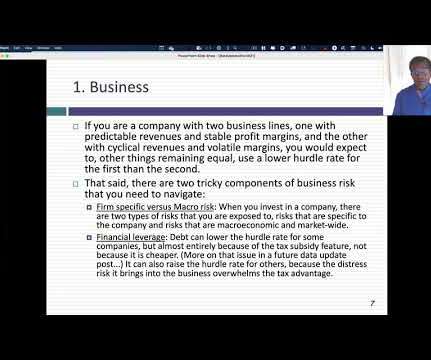

In my last three posts, I looked at the macro (equityriskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

The first is to see how the increase in inflation in 2021 and 2021 has played out in profitability for companies, since inflation can increase profits for some firms, and lower them for others. It was in attempting to estimate the latter that I computed the costs of equity in my second post and costs of capital in my third.

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. Source Data The two estimates move together much of the time, but the consumer expectations are consistently higher, and at the end of April 2021, the consumer survey was forecasting inflation of 3.2%, about 1.1%

Zomato, an Indian online food-delivery company, was opened up to public market investors on July 14, 2021, and its market debut is being watched for clues by a number of other online ventures in India, waiting in the wings to go public. The service was initiated in 2017 and it had 1.5

A few of you did take issue with the fact that the growth rate that I used for the first five years dropped from 35%, in my November 2021 valuation , to 24%, in my most recent one. There is not much room to maneuver on either number, since half of all US companies have costs of capital between 7.3% It was the reason that I argued at a $1.2

pm (New York time) All three classes start on February 1, 2021 and end on May 10, 2021. The class times for the coming semester are below: Corporate Finance: Mondays & Wednesdays, 12.30 pm (New York time) Valuation (MBA): Mondays & Wednesdays, 2.00 pm (New York time) Valuation (Undergraduate): Mondays & Wednesdays, 3.30

She recently received the 2021 LCPA Women to Watch Most Experienced Leader Award. He is a frequent presenter on valuation topics, and is currently a subject matter expert on the Appraisal Foundation’s working group preparing a Valuation Advisory on the Company-Specific RiskPremium. Tax Valuation Services.

With stocks, I compute this pre-personal tax return at the start of every month, using the current level of index and expected cash flows to back out an internal rate of return; this is the basis for the implied equityriskpremium.

Just to illustrate the contradictions that can result, PRS gives Libya a country risk score that is higher (safer) than the scores it gives United States or France, putting them at odds with most other services that rank Libya among the riskiest countries in the world.

billion invested in Russian equities on February 23, 2022 , almost all of which was wiped out during the next few weeks. Risk Surge and Economic Viability : In my last post, I noted the surge in Russia's default spread and country riskpremium, making it one of the riskiest parts of the world to operate in, for any business.

Thus, the answer to questions about past interest rate movements (the low rates between 2008 and 2021, the spike in rates in 2022) as well as to where interest rates will go in the future has been to look to central banking smoke signals and guidance. They made a mild comeback in 2023 and that recovery continued in 2024.

Strong empirical evidence shows the United States has a lower cost of equity capital than comparable countries and that this lower cost is attributable in part to an institutional design that protects the independence of securities regulators and assures strong enforcement. In the United States, the cost of capital is lower than elsewhere.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equityriskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content