This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Leading into 2021, the big questions facing investors were about how quickly economies would recover from COVID, with the assumption that the virus would fade during the year, and the pressures that the resulting growth would put on inflation.

Highlights: End markets mature, no opportunities to grow. Massive dividend yield secured by strong cash generation. In July 2021, the stock price faced a sharp drop by more than 30%. Cash machine ensures consistent massive dividend yield. The FCF yield shows ROEC’s dividend-paying potential.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Return on (invested) capital 2.

The notion of computing a cost of capital for a bank is fanciful and fruitless, and any attempt to compute an enterprise value for a bank is destined to end in failure. The other was that the bank regulatory framework operated effectively , preventing banks from overreaching on risk or being under capitalized.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms.

In 2021, looking at the company, I feel more convinced than I was a few years that it is, at its core, an automobile company, and while it will continue to derive revenues from batteries and perhaps even software, its pathway to becoming a trillion dollar market cap company still runs through the "car company" story.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. It is also why I report only aggregated data on industries, rather than company-level data.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

That positive result notwithstanding, the recovery was uneven, with a big chunk of the increase in marketcapitalization coming from seven companies (Facebook, Amazon, Apple, Microsoft, Alphabet, NVidia and Tesla) and wide divergences in performance across stocks, in performance. increase in marketcapitalization.

Investors, used to a decade of better-than-expected earnings and rising stock prices at these companies, have been blindsided by unexpected bad news in earnings reports, and have knocked down the marketcapitalization of these companies by hundreds of billions of dollars in the last few weeks.

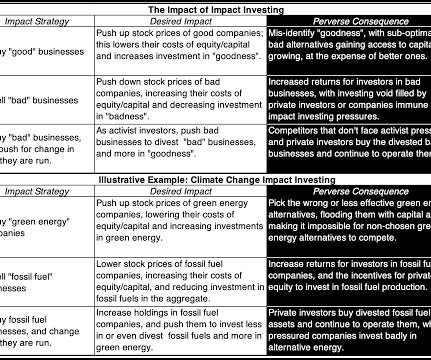

trillion was invested by impact investors in 2021, with a diverse range of investors: Global Impact Investing Network, 2022 Report Not surprisingly, the balance between social impact and financial return desired by investors, varies across investor groups, with some more focused on the former and others the latter.

While management decisions have clearly contributed to the problems, it is also true that the pharmacy business, which forms Walgreen's core, has deteriorated over the last two years, and that can be seen by comparing its market performance to CVS, its highest profile competitor. That acquisition, which cost Walgreens $5.2

That said, about 31% of the net profits of all publicly traded firms listed globally in 2021 were generated by financial service firms; that percent is lower in the US and higher in emerging markets.

If anything, the economy seems to have settled into a stable pattern, albeit at the high levels that it reached in the second half of 2021. I know that the game is not done, and the long-promised pain may still arrive in the second half of the year, but for the moment, at least, markets have found some respite.

ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. Currently the company is trading at CHF 30 per share with a marketcapitalization of CHF 56.1 At this level the dividend yield is 2.8%. . In comparison to ABB’s marketcapitalization of CHF 56.1

ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. Currently the company is trading at CHF 30 per share with a marketcapitalization of CHF 56.1 At this level the dividend yield is 2.8%. . In comparison to ABB’s marketcapitalization of CHF 56.1

In this post, I want to focus on that point, starting with a discussion of why stories matter to investors and traders and the story that propelled the company to a trillion-dollar marketcapitalization not that long ago. The reason is simple. Facebook: A Narrative Reset?

Two weeks ago TotalEnergies announced its net income for the third quarter of 2022 which increased by 43% compared to 2021 and amounted to €6.6 This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%.

Two weeks ago TotalEnergies announced its net income for the third quarter of 2022 which increased by 43% compared to 2021 and amounted to €6.6 This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%.

07 Question: In each of 2020 and 2021, a registrant provided the same list of companies as a peer group in its Compensation Discussion & Analysis (“CD&A”) under Item 402(b) but provided a different list of companies in its CD&A for 2022. In what circumstances is such marketcapitalization-based weighting required?

Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world. At the company-level, I provide data on risk, profitability, leverage and dividends, broken down by industry-groups, to be used in both corporate finance and valuation. Return on Equity 1.

This was primarily based on revenue growth, which registered a heady 30% rise, allowing the bank to distribute its highest full-year dividend since 2008. The group’s marketcapitalization in 2023 was at a 17-year high, valuing the enterprise at around the same level in dollar terms as Goldman Sachs. billion in 2022.

For example, market makers generate quotations for exchange-listed options by deriving their value from real-time stock prices and five additional factors: exercise price, the risk-free interest rate, time to expiration, volatility of the stock, and dividends. 3 (2021). [8] 4] Unger v. Amedisys [5] and Krogman v. 1264 (D.N.J.

In a predictable consequence, US multinationals chose to leave their foreign income outside the US, creating the phenomenon of trapped cash, i.e., income held in foreign locales to avoid taxes, but also trapped because that income could not be used to pay dividends, buy back stock or invest in projects in the United States.

For Microsoft, this would yield values of $69,916 million for operating income and an effective tax rate of 13.83% in 2021, resulting in a FCFF of $40,879 million in 2021. An intuitive reading of the FCFE is that it is cash available to be returned to equity investors, either in the form of dividends or as cash buybacks.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like marketcapitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

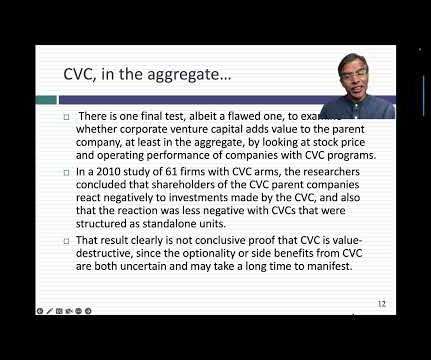

Put simply, there are relatively few firms, where there is corporate venture capital arm or division, that is in charge of, and accountable for, CVC investments. Over its lifetime, Google Ventures has picked some big winners, including iUber, Airbnb and Slack, all of which are now public companies with substantial marketcapitalization.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content