This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Consequently, you can only value the equity in a bank, and by extension, the only pricing multiples you can use to price banks are equity multiples (PE, Price to Book etc.). The notion of computing a cost of capital for a bank is fanciful and fruitless, and any attempt to compute an enterprisevalue for a bank is destined to end in failure.

Example: Here’s an example of a particular metric you might use: In order to determine the EnterpriseValue of the business, you find the EBITDA from the business you’re valuing, and then multiply this by the EBITDA multiple observed from the other comparable companies. SaaS start-ups are valued at 10x Sales”.

Example: Here’s an example of a particular metric you might use: In order to determine the EnterpriseValue of the business, you find the EBITDA from the business you’re valuing, and then multiply this by the EBITDA multiple observed from the other comparable companies. SaaS start-ups are valued at 10x Sales”.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms.

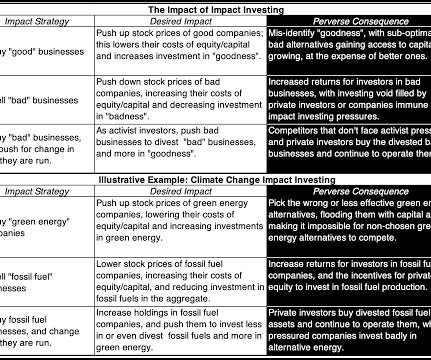

trillion was invested by impact investors in 2021, with a diverse range of investors: Global Impact Investing Network, 2022 Report Not surprisingly, the balance between social impact and financial return desired by investors, varies across investor groups, with some more focused on the former and others the latter.

At the company-level, I provide data on risk, profitability, leverage and dividends, broken down by industry-groups, to be used in both corporate finance and valuation. Financing Flows Accounting Returns Dividends & Ownership Risk Premiums 1. Dividend Payout & Yield 1. Dividends/FCFE & (Dividends + Buybacks)/ FCFE 2.

VAALCO to acquire, through an indirect wholly-owned subsidiary, each TransGlobe share for 0.6727 of a VAALCO share; Implied TransGlobe equity value of US$307 million (with premium), and enterprisevalue of US$273 million assuming cash of US$37 million and debt of US$3 million as of March 31, 2022; A 24.9 percent and 45.5

For Microsoft, this would yield values of $69,916 million for operating income and an effective tax rate of 13.83% in 2021, resulting in a FCFF of $40,879 million in 2021. An intuitive reading of the FCFE is that it is cash available to be returned to equity investors, either in the form of dividends or as cash buybacks.

(NASDAQ: PYCR ) in an all-cash transaction representing an enterprisevalue of around $4.1 billion and took the company public in July 2021. Paychex plans to maintain its dividend policy and strong balance sheet, with committed financing in place for the. Paychex will acquire Paycor for $22.50

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like market capitalization or enterprisevalue) as recently as ten years ago, and barely making the top ten list five or six years ago.

Growth Equity Interview Questions: Technical Concepts As with private equity interviews , they could potentially ask you about anything: Accounting , equity value and enterprisevalue , valuation and DCF analysis , and even merger models and LBO models. Explain how the Equity Value, EnterpriseValue, and ownership change.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content