This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Dividend yield & payout 3. Buybacks 2.

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. So another major assumption when adopting this method, is that the type of ratio chosen as the comparison point, such as P/E or EV/EBITDA should be similar across similar firms. .

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. So another major assumption when adopting this method, is that the type of ratio chosen as the comparison point, such as P/E or EV/EBITDA should be similar across similar firms. .

That said, about 31% of the net profits of all publicly traded firms listed globally in 2021 were generated by financial service firms; that percent is lower in the US and higher in emerging markets.

By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time. For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive.

Adjusted EBITDA and EPS Guidance Affirmed, Outlook Updated to Reflect FX Translation Global Restructuring Expected to Yield $40 Million in Profit Growth in 2023 Balanced Capital Allocation Strategy Includes NoteMachine Acquisition and Continued Share Repurchases. GAAP net income up 1% to $19 M; adjusted EBITDA up 11% to $189 M.

growth in Funds From Operations per diluted share (2022 vs. 2021) 4.6% increase in same-center cash net operating income (2022 vs. 2021) 98.1% net principal debt-to-annualized EBITDA ratio for 4Q‘22 (vs. growth in Funds From Operations per diluted share (2022 vs. 2021) 4.6% million gain on sale of real estate during 2021.

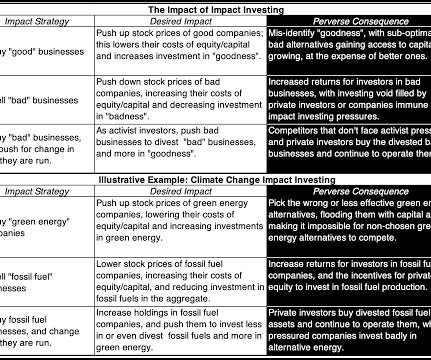

trillion was invested by impact investors in 2021, with a diverse range of investors: Global Impact Investing Network, 2022 Report Not surprisingly, the balance between social impact and financial return desired by investors, varies across investor groups, with some more focused on the former and others the latter.

Two weeks ago TotalEnergies announced its net income for the third quarter of 2022 which increased by 43% compared to 2021 and amounted to €6.6 This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. Recent Financial Performance.

ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. At this level the dividend yield is 2.8%. . The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E.

ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. At this level the dividend yield is 2.8%. . The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E.

Two weeks ago TotalEnergies announced its net income for the third quarter of 2022 which increased by 43% compared to 2021 and amounted to €6.6 This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. Recent Financial Performance.

per diluted share for the same period in 2021. versus the same period in 2021. per diluted share for the same period in 2021. per diluted share for the same period in 2021. per diluted share, for the same period in 2021. compared to the same period in 2021. September 30, 2021. million , or $0.13

Q1 2022 consolidated Adjusted EBITDA (as defined and reconciled below) of $87.0 The effect of the series of transactions in the last couple of quarters as well as continued focus on operational cost resulted in sequential Adjusted EBITDA 8% greater than Q4 2021. million, a decrease of 17% compared to the fourth quarter of 2021.

These cross-selling synergies, alongside those related to operating costs, are expected to accelerate once we complete the integration, reaching an annual run rate in excess of $170 million over the next three to five year period, enhancing EBITDA and free cash flow growth.

The Transaction implies a multiple of less than 9x the projected forward Adjusted EBITDA and is immediately accretive, with DCF per share accretion in the mid-teens 4 , 5 , 6. In March 2021, STGT completed the final construction phase of incremental storage facilities bringing the total terminalling capacity to 8.6

Your answer to that question will determine not just how you approach running the business, but also the details of how you pick investments, choose a financing mix and decide how much to return to shareholders, as dividend or buybacks.

Venture capitalist, raised on a diet of big stories and total addressable markets has little in common with bankers, trained to think in terms of EV to EBITDA multiples and accounting ROIC, and when put in a room together, it should come as no surprise that they find each other's language indecipherable. The reason is simple.

billion in sales and adjusted EBITDA of $340 million, an increase of 47% compared to the $232 million of adjusted EBITDA generated during fiscal year 2021. For fiscal year 2022, Worthington's Consumer Products, Building Products and Sustainable Energy Solutions businesses delivered $1.3

Combined Company targeting a low teen Adjusted EBITDA CAGR through 2023 from a 2021 base of $305 million 1. billion of Revenue and $305 million of Adjusted EBITDA in 2021 4. 2021 Combined Company Revenue. ($ in millions). Combined Company Adjusted EBITDA. ($ in millions). Combined Company had $2.7

A good example is the 2020 – 2021 period, when SPAC activity went vertical, and plenty of renewable energy companies used SPACs to go public. If you look at the presentations and valuations below, you will still see standard valuation multiples like TEV / Revenue, TEV / EBITDA, and P / E.

In the last two decades, I have seen free cash flow measures stretched to cover adjusted EBITDA, where stock-based compensation is added back to EBITDA, and with WeWork, to community-adjusted EBITDA, where almost all expenses get added back to get to the adjusted value.

The company's return on invested capital has steadily declined, even as it has scaled up, hovering just over 3% in 2021-2022. The interest coverage ratio better captures the limited buffer that the company has on its debt load, since the operating income is barely higher than interest expenses. times revenues in the most recent two years.

billion market cap that trades at 7x trailing revenue on expected revenue growth rates of 15 – 20% and projected EBITDA margins of ~20%. So, most of the returns will have to come from EBITDA growth, with a small amount coming from Cash generated during the holding period (if any). A 2x multiple over 5 years is a 15% IRR.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content