This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These final rules follow the SEC’s issuance of proposed rules in July 2015, which laid dormant until the re-opening of two separate comment periods in October 2021 and June 2022. – Excludes revisions due to internal reorganizations impacting reportable segment disclosures or changes in capitalstructure (e.g.,

Accordingly, the charters of companies with dual-class structures often provide that any “transfer” (broadly defined) by the original high-vote stockholders will result in automatic conversion of the transferred shares into the company’s ordinary, low-vote shares. [1]

Janus International Group (NYSE: JBI ), a provider of custom building product solutions and access control technologies within the self-storage sector of the commercial real estate industry, is observing its first anniversary as a publicly-traded company since merging with blank-check company Clearlake Capital Group on June 7, 2021.

(OTC: SIRC ), an integrated, single-source solutions provider of solar power, roofing and EV charging systems, today announced the acquisition and retirement of its outstanding Class C Preferred Stock associated with the 2021 Enerev acquisition. Holmes, Chairman and Chief Executive Officer of Solar Integrated Roofing Corp.

Consider research done by Kroen (2021) that shows that since about 1998, U.S. Chart from Kroen (2021). This usually happens when a company is making a deliberate and significant change to its capitalstructure. companies have distributed more money through buybacks than through dividends.

2022 saw a robust cash and capitalstructure with a staggering USD 967 million adjusted EBITDA in Q4, up by 14% from the previous year. With the economic recovery in 2021 and a resurgence in energy demand, Oneok’s operations and financial performance improved, leading to a rebound in its share price. per share.

18] Certain features of modern-day distressed capitalstructures exacerbate this problem. June 12, 2021, 5:30 AM), [link] ; Sujeet Indap & Mark Vandevelde, Hedge Fund Executive Sentenced to 6 Months in Jail for Bankruptcy Fraud , Fin. Times (May 7, 2021), [link]. [4] 1333 (2021); Jared A. 363, 368 (2021). [8]

workforce, while, in 2021, hedge funds managed assets exceeding a staggering $4 trillion. While the ownership structures implemented by these firms differ, they generally encourage active engagement with portfolio companies. By 2022, firms under private equity management employed over 11 million people, nearly 10 percent of the U.S.

The SPAC Boom and Subsequent Contraction Most of today’s de-SPACed companies are the result of the boom in SPAC fundraisings in 2020 and 2021, when there were 861 SPAC initial public offerings (IPOs), accounting for more than half of all IPOs in both years. 3 The SPAC IPO market began to wane in late 2021 and contracted further in 2022.

11] Data collected indicates that an average of 58% of SPAC IPO shareholders redeemed in 2020-2021, [12] and reporting indicates that redemptions from the first quarter of 2022 are higher. [13]. 14, 2021). [2] 9, 2021). [4] 14, 2021). [2] 9, 2021). [4] 2021-09); Eric Ver Ploeg, Tech SPAC Redemption Rates (Jan.

Restructuring is a complex and multi-dimensional process that involves a range of actions affecting operations, capitalstructure, and governance. The existing theories of zombie lending largely rely on regulatory capital requirements (Caballero et al., 2008; Peek and Rosengren, 2005). and Yang, Y., Available at SSRN 3910214.

In the United States, the debate in the corporate governance literature about the economic perils of dual-class capitalizationstructures is completely disconnected from rising concerns over outsized political influence of the tech industry among some antitrust thinkers and politicians. 26, 2022. [2] 116-222, 134 Stat. 4] Ronald J.

Belk had its plan of reorganization confirmed on February 23, 2021. The company’s financial creditors, institutions that held first-lien debt and second-lien debt, negotiated with the company and its private equity sponsor for months over a new capitalstructure. Belk had been taken private in a leveraged buyout in 2015.

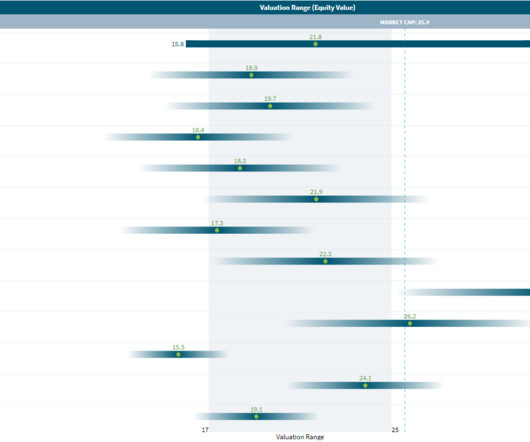

It is often used as it eases the comparability between companies from the same industry (without having to worry about asset or capitalstructure). . This is a very similar multiple to the EV/EBITDA excludes D&A (thus the asset structure). EV/EBITDA – Shows the ratio of Enterprise Value to the EBITDA of a company.

It is often used as it eases the comparability between companies from the same industry (without having to worry about asset or capitalstructure). . This is a very similar multiple to the EV/EBITDA excludes D&A (thus the asset structure). EV/EBITDA – Shows the ratio of Enterprise Value to the EBITDA of a company.

Different Buyback Rationales – and Their Implementation Objectives We will consider each of the three corporate finance-based rationales for buybacks, being investment, capital restructuring and excess capital return or dividend. 7] Cliff Asness co-founder of AQR – The Illiquidity Discount?

27] Unitranche Debt The other trend in private credit financing arrangements is the rise of single-tranche or unitranche loans, which eliminate the complex capitalstructure of first- and second-lien debt in favor of a single facility. [28] 18] maximum expenditure on capital assets for a given period. [19]

As SPAC IPOs broke records – in both value and volume – in 2020 (and again in 2021), it was inevitable that stockholder litigation would follow. More than 50% of the SPACs that went public in 2020 and 2021 are incorporated in Delaware, giving particular significance to SPAC litigation filed in Delaware courts.

The aim of a downgrade is to communicate supervisory concerns to the bank and to serve as a warning that enforcement actions could be in the offing, see Bergin and Stiroh (2021). [8] Thus, structured disclosure is not subject to an endogeneity critique, e.g., Bond and Goldstein (2014). [23] 19] Similarly, Berger, et al.

She recently received the 2021 LCPA Women to Watch Most Experienced Leader Award. He has over 15 years of experience in valuation engagements for public and private companies in support of tax, business combinations, impairment testing, stock-based compensation, reorganizations, and claims within complex capitalstructures.

5] As Healy described it, failures at funds included 1) disregard of fiduciary standards, 2) lack of regulation of investment advisers, 3) complicated capitalstructures, 4) inadequate accounting, and 5) lack of supervision of mergers and consolidations. [6] 15, 2021), available at [link]. 27, 2021), available at [link]. [28]

For Microsoft, this would yield values of $69,916 million for operating income and an effective tax rate of 13.83% in 2021, resulting in a FCFF of $40,879 million in 2021. During the 2021 fiscal year, Microsoft bought Nuance Communications for $19.76

PTMN and LRFC employ the same investment strategy, and the BC Partners Credit Platform has been allocating substantially similar or the same investments to both Companies since Mount Logan Management, LLC ("Mount Logan") became LRFC's external investment adviser on July 1, 2021.

The case was moot, plaintiffs-appellees argued, because, following the conversion, Holdings had merged with and into Tripadvisor, leaving Tripadvisor with a simplified capitalstructure and no controlling stockholder. [4] 2021) (noting that the extreme language in Synthes should not be read as establishing a general rule). [19]

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content