This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

“Under any standard of value, the true economic value of a business enterprise will equal the company’s accounting bookvalue only by coincidence.” So why do so many shareholder buy-sell agreements require that the shares be purchased for bookvalue? Neville, Rodie and Shaw, Inc. 16, 2024) is the latest.

The threshold for certain pre-closing net benefit reviews under the Investment Canada Act (ICA) and the threshold for a pre-closing merger notification under the Competition Act have now both been released for 2021. It is adjusted annually, and for 2021 the threshold is C$415 million, down from C$428 million in 2020.

That said, about 31% of the net profits of all publicly traded firms listed globally in 2021 were generated by financial service firms; that percent is lower in the US and higher in emerging markets. To make comparisons, profits are scaled to common metrics, with revenues and bookvalue of investment being the most common scalar.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms. Data Update 2 for 2021: The Price of Risk!

Price to Book Ratio: Choice and Drivers There is no sector where price to book ratios get used more than in banking and financial services, for two reasons. To use the price to book ratio to price banks, I begin by identifying its drivers, and that is simple to do, if you start with an intrinsic equity valuation model.

One way to measure progress on this issue is to look at the portion of the bookvalue of equity at US companies that comes from tangible assets, in the chart below: Looking across all US firms from 1980 to 2022, the portion of bookvalue of equity that comes tangible assets has dropped from more than 70% in 1998 to about 30% in 2022.

Standard Deviation in Equity/Firm Value 2. BookValue Multiples 3. Working capital needs Thus, I compute pricing multiples based on revenues (EV to Sales, Price to Sales), earnings (PE, PEG), bookvalue (PBV, EV to Invested Capital) or cash flow proxies (EV to EBITDA). Fundamenal Growth in Operating Earnings 3.

The second is that the sanctions imposed after 2021 on doing business in Russia drove foreign competitors out of the market, leaving the market almost entirely to domestic companies. The first is the preponderance of natural resource companies in this region, and energy companies had a profitable year in 2023.

Apollo Bank operates five branches across Miami-Dade County with deposits of approximately $928 million and loans of $665 million as of December 31, 2021. Seacoast's South Florida presence has grown in recent years, including through its acquisition of Legacy Bank of Florida in 2021. Seacoast expects the transaction to be 8.0%

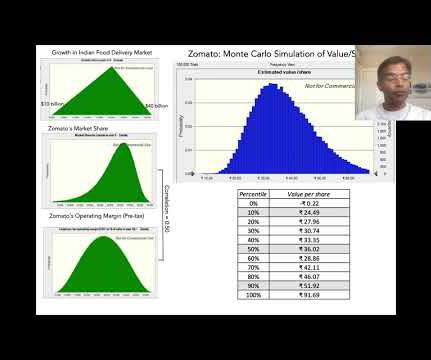

Zomato, an Indian online food-delivery company, was opened up to public market investors on July 14, 2021, and its market debut is being watched for clues by a number of other online ventures in India, waiting in the wings to go public. The service was initiated in 2017 and it had 1.5

First Quarter 2022 Results (All comparisons refer to the fourth quarter of 2021, except as noted). per diluted share during the fourth quarter of 2021. The allowance for credit losses as a percentage of total loans totaled 1.04%, compared to 1.10% at December 31, 2021. at December 31, 2021. for the full year 2021.

The Williams Companies decision [7] in 2021 indicated that the Delaware judiciary will view unusual features of a pill directed at shareholder activism with considerable skepticism. A Japanese Supreme Court decision in 2021 is the most significant and potentially troubling from a doctrinal standpoint. [9] 26, 2021), aff’d sub nom.

In 2021, it sold more than 100,000 battery electric vehicles (BEV). The company missed its 2021 sales target by 4% amid the chip crisis. Bookvalue is the value attributable to shareholders in case the company sells all its assets and repays its liabilities (also called liquidation value).

Price/Book : This multiple compares the price to the bookvalue of a firm. For example, if I use the P/E multiple, I should use the Earnings of the comparable companies for the same year (say 2021) as for my target company. It shows the amount an investor is willing to pay for one dollar of net earnings. .

Price/Book : This multiple compares the price to the bookvalue of a firm. For example, if I use the P/E multiple, I should use the Earnings of the comparable companies for the same year (say 2021) as for my target company. It shows the amount an investor is willing to pay for one dollar of net earnings. .

The first is to see how the increase in inflation in 2021 and 2021 has played out in profitability for companies, since inflation can increase profits for some firms, and lower them for others. In this post, I will focus on trend lines in profitability at companies in 2022, with the intent of addressing multiple questions.

20] Regarding fair price, the Second Circuit found Tilton’s valuation method of NewCo neglected the “highest value reasonably available under the circumstances.” [21] 20-CV-06274 (LAK), 2021 WL 4459733, at *9 (S.D.N.Y. 29, 2021), aff'd , 81 F.4th 8] PPAS would then sell those assets to Tilton affiliates. [9] 548(a)(1)(A). [2]

By early 2021, the industry had effectively made a full recovery in spite of supply chain and inventory challenges and M&A activity in this space rebounded accordingly, with a record 383 transactions completed in 2021, and an estimated 374 transactions completed in 2022. Despite larger U.S. Cash and Other Working Capital.

The Transaction emerged through continued dialogue with MacKellar over the past two years, following NACG's entry into Australia through the acquisition of DGI Trading Pty Limited in 2021. The Transaction is fully funded by bank secured & vendor provided debt financing.

Direct Line's brokered Commercial Lines generated written premiums 4 of £530 million in 2022, and delivered an average combined ratio 5 6 of approximately 96% across 2021 and 2022. The transaction will result in the transfer of renewal rights, brands, employees, and systems to RSA.

Since net income increases by the same magnitude, the company generated $42.5 billion in net income in the last twelve months, if you correct for R&D, rather than $28.8 billion , as reported. We are certain that while some of these reality-lab related expenses are operating, a large portion represent capital expenses that are being expensed.

If anything, the economy seems to have settled into a stable pattern, albeit at the high levels that it reached in the second half of 2021. In 2022, old-time value investors felt vindicated, as the damage that year was inflicted on the highest growth companies, especially in technology.

For example, I have seen it asserted that a stock that trades at less than bookvalue is cheap or that a stock that trades at more than twenty times EBITDA is expensive. Check rules of thumb : Investing and corporate finance are full of rules of thumb, many of long standing.

Bookvalue per common share of $22.79 Tangible bookvalue per common share of $20.38 During first quarter 2023, Salisbury did not repurchase any of its outstanding common stock pursuant to its stock repurchase program, which was established in March 2021 and renewed in March 2022. million at March 31, 2023.

The company's return on invested capital has steadily declined, even as it has scaled up, hovering just over 3% in 2021-2022. You see similar movements in the price to book, where the stock has gone from trading under bookvalue to 6.7 times revenues in the most recent two years.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content