This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

In a third post on July 1, 2022 , I pointed to inflation as a key culprit in the retreat of risk capital, i.e., capital invested in the riskiest segments of every market, and presented evidence of the impact on riskpremiums (bond default spreads and equity riskpremiums) in markets.

Inflation: The Full Story I wrote my first post on this blog in 2008, and inflation merited barely a mention until 2020, though it is an integral component of investing and valuation. Just as important, though, is the fact that variation in inflation, from year to year, was lower in 2011-2020 in every other decade, other than 1991-2000.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

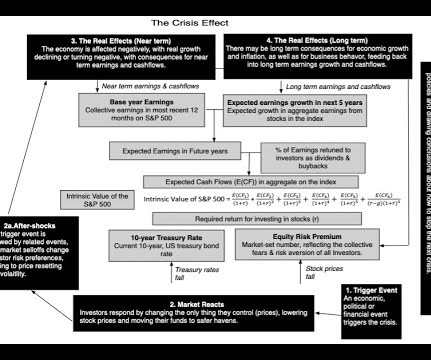

Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums. It is true that economists have researched risk aversion for centuries and concluded that investors are collectively risk averse, and that the level of risk aversion varies across age groups, income levels and time.

Exacerbating the pain, corporate default spreads rose during the course of 2022: While default spreads rose across ratings classes, the rise was much more pronounced for the lowest ratings classes, part of a bigger story about risk capital that spilled across markets and asset classes. US Equities in 2023: Into the Weeds!

The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.” The riskpremium reflects that market participants require compensation for taking on uncertainty. The riskpremium may incorporate factors such as credit risk or market illiquidity.

Just as rising equity riskpremiums push up the cost of equity, rising default spreads push up the cost of debt of companies, with the added complication of higher default risk for those companies that had pushed to the limits of their borrowing capacity in a low interest-rate environment.

My two most recent valuations were in June 2019 and January 2020, and I am going to go back to them, not just because they are recent, but because they led to investment decisions on my part. Between June 2019 and January 2020, the stock went on a tear, as the stock price more than tripled, and I revisited my Tesla valuation.

Beta & Risk 1. Equity RiskPremiums 2. I also have implied equity riskpremiums (forward-looking and dynamic estimate of what investors are pricing stocks to earn in the future) for the S&P 500 going back annually to 1960 and monthly to 2008, and equity riskpremiums for countries. Buybacks 2.

Corporate Bonds: No Shortage of Risk Capital In my last post, I chronicled the movement in the equity riskpremium, i.e. the price of risk in the equity market, during 2021, but the bond market has its own, and more measurable, price of risk in the form of corporate default spreads.

The answer, to me, seems to be obviously yes, though there are still some who argue otherwise, usually with the argument that country risk can be diversified away. In that post, I computed the equity riskpremium for the S&P 500 at the start of 2021 to be 4.72%, using a forward-looking, dynamic measure. as mature markets.

Tesla's rise is summarized in the graph below, where we look at the company's revenues and earnings over time, with earnings measured in gross and operating terms, and EBITDA capturing operating cash flows: 2022 numbers updated to reflect 4th quarter earnings call on 1/25/23 Between 2010 and 2020, Tesla grew revenues from $117 million to $31.5

Revenues did drop in 2020, as COVID restrictions put a crimp on the restaurant business, but the quarterly data suggests that business is coming back. That number was 23.13% in FY 2020, but dropped to 21.03% in FY 2021, as shut downs put a crimp on business.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

As the economy climbs back from the shutdown in 2020, there are some who argue that the monetary and fiscal stimuli of the last year, unprecedented though they may be in size and scale, will not cause inflation because the economy has substantial excess capacity. Louis estimates for inflation rates exceeding 2.5%

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

I also offer online classes in basic finance (present value, risk models and measures) and accounting (or at least my version of it) as background to my main classes. Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.

In 2020, in full recognition of his outstanding services in the Society and contributions to the appraisal profession, the American Society of Appraisers gave him their Lifetime Achievement Award. He was a on the Board of Trustees of the International Valuation Standards Council finishing his second term in 2023.

If equity markets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equity markets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

And Consequences If you are wondering why you should care about risk capital's ebbs and flows, it is because you will feel its effects in almost everything you do in investing and business. That pullback has had its consequences, with equity riskpremiums rising around the world.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

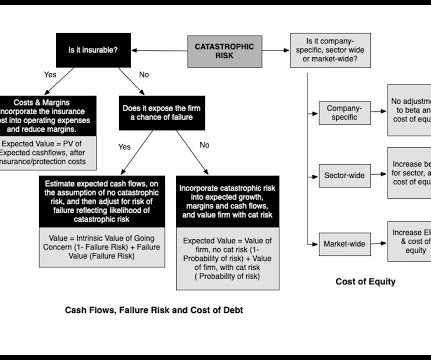

In some cases, a change in regulatory or tax law can put the business model for a company or many company at risk. I confess that the line between whether nature or man is to blame for some catastrophes is a gray one and to illustrate, consider the COVID crisis in 2020. Note that these higher discount rates apply in both scenarios.

Those measures took a beating in 2020, as COVID decimated the earnings of companies in many sectors and regions of the world, and while 2021 was a return to some degree of normalcy, there is still damage that has to be worked through. Louis, FRED , which contains historical data on almost every macroeconomic variable, at least for the US.

Coming in 2020, the ten-year T.Bond rate at 1.92% was already close to historic lows. The arrival of the COVID in February 2020, and the ensuing market meltdown, causing treasury rates to plummet across the spectrum, with three-month T.bill rates dropping from 1.5% In particular, the Fed's own assessments of real growth of 6.5%

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. In computing the latter, I used the current debt ratios for firms, but made no attempt to evaluate whether these mixes were "right" or not.

At first sight, stocks have had an impressive run over much of the last century, delivering substantial return premiums over treasury bonds, treasury bills and corporate bonds: Historical returns on stocks, bonds and bills: 1928 -2020 These returns, though, are prior to personal taxes, and the tax bite can be substantial.

In the language of risk, they are demanding higher prices for risk, translating into higher riskpremiums. Those equity riskpremiums did not get back to pre-2008 levels until almost 15 years later.

While it is true that the Fed became more active (in terms of bond buying, in their quantitative easing phase) in the bond market in the last decade, the low treasury rates between 2009 and 2020 were driven primarily by low inflation and anemic real growt h. Put simply, with or without the Fed, rates would have been low during the period.

NYU Business School Professor Damoradans widely used valuation data, for example, currently shows the United States as having among the lowest equity riskpremiums in the world. [3] Bank of England Working Paper (2020). In the United States, the cost of capital is lower than elsewhere. 485 (2004); N. Fraccaroli, R. Coffee, Jr.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content