This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In 2022, we needed that reminder more than ever before, especially after markets came roaring back from the COVID drop in 2020 and 2021. We invest in equities expecting to earn more than we can make on riskfree or guaranteed investments, but the risk in equities is that actual returns can deviate from expectations.

Put simply, no central bank, no matter how powerful, can force market interest rates down, if inflation expectations stay low, or up, if investor are anticipating high inflation. Note that the decrease in default spreads, at least for the lower ratings, mirrors the drop in the implied equityrisk premium during the course of 2021.

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of risk premiums.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors.

My two most recent valuations were in June 2019 and January 2020, and I am going to go back to them, not just because they are recent, but because they led to investment decisions on my part. Between June 2019 and January 2020, the stock went on a tear, as the stock price more than tripled, and I revisited my Tesla valuation.

Inflation: The Full Story I wrote my first post on this blog in 2008, and inflation merited barely a mention until 2020, though it is an integral component of investing and valuation. In fact, the average inflation rate in the 2011-20 decade was the lowest of the seven decades that I cover in this chart.

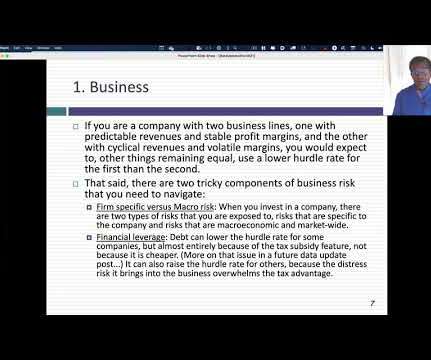

Cost of raising funds (capital) : Since the funds that are invested by a business come from equity investors and lenders, one way in which the hurdle rate is computed is by looking at how much it costs the investing company to raise those funds. But what if the company is looking at a project in Nigeria or Bangladesh? for Ford).

In my last three posts, I looked at the macro (equityrisk premiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Tesla's rise is summarized in the graph below, where we look at the company's revenues and earnings over time, with earnings measured in gross and operating terms, and EBITDA capturing operating cash flows: 2022 numbers updated to reflect 4th quarter earnings call on 1/25/23 Between 2010 and 2020, Tesla grew revenues from $117 million to $31.5

Gazprom’s revenue breakdown 2020. Its net-debt to equity ratio stood at 0.3 Russia has a massively high risk-freerate of 10%. Highlights: Bright future of natural gas as a transition fuel. If Europe holds back Gazprom expansion, pivot to Asia. Domestic market still not fully penetrated yet. Ratios – Gazprom.

The first is the spike in the Fed Funds rate to more than 20% between 1979 and 1982, when Paul Volcker was Fed Chair, and represented his attempt to break the cycle of high inflation that had entrapped the US economy.

Idemitsu Kosan’s revenue breakdown 2020. Its net-debt to equity ratio stood at 0.9x Historically, Japan has a very low risk-freerate. Ramp-up of CAPEX necessary to ensure longevity. Attractive dividend yield could rise to 2x Japanese average. Download the full report as a PDF. The share price is up 33% YTD.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

I also offer online classes in basic finance (present value, risk models and measures) and accounting (or at least my version of it) as background to my main classes. Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. for 2021 and inflation of 2.2%

Those measures took a beating in 2020, as COVID decimated the earnings of companies in many sectors and regions of the world, and while 2021 was a return to some degree of normalcy, there is still damage that has to be worked through.

While it is true that the Fed became more active (in terms of bond buying, in their quantitative easing phase) in the bond market in the last decade, the low treasury rates between 2009 and 2020 were driven primarily by low inflation and anemic real growt h. They made a mild comeback in 2023 and that recovery continued in 2024.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content