This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

economy for most of 2020 and causing an unprecedented economic impact on small businesses, DealStats Value Index (DVI) captured the 12-month snapshot on how earnings before interest, taxes, depreciation, and amortization (EBITDA) multiples have trended. With the COVID-19 pandemic putting a stranglehold on the U.S.

Click to Download: Middle Market Private Equity M&A Activity – Q2 2020 Executive Summary Transaction Volume Shrinks Only 31 transactions were reported in Q2 2020, bringing the total reported transactions in 2020 to 113. Debt Usage Decline In Q2 2020, total debt to EBITDA fell to 3.3x in 2020 from 8.4x

Click to Download: Middle Market Private Equity M&A Activity – Q2 2020. Only 31 transactions were reported in Q2 2020, bringing the total reported transactions in 2020 to 113. In Q2 2020, total debt to EBITDA fell to 3.3x Despite the simple average enterprise value (EV) to EBITDA multiple remaining at 7.4x

The EBITDA multiples in 2021 not only reached, but much exceeded pre-pandemic levels. It is too early to determine the reasons why the EBITDA multiple for footwear companies surpasses 33X, while the multiple for MedTech firms exceeds 35X. High EBITDA multiples, on the other hand, may be viewed as a way to discount inflation.

After the trials and tribulations of 2020, no one really knew what to expect going into 2021. Last year has most certainly been a record year for M&A deals, making a huge comeback from 2020. That’s up an unprecedented 24% from 2020. Almost all sectors are showing signs of recovery from 2020.

3] The Grant On January 21, 2018, Tesla’s Board of Directors (the “Board”) [4] unanimously approved the Grant, which would vest based on Tesla’s achievement of certain market capitalization goals, as well as operational milestones related to revenue and adjusted EBITDA targets. The process arrived at an unfair price.” [3]

With all the changes made to the Code in 2020 due to COVID-19, it is worthwhile to review Code Sec. ATI was defined as EBITDA, that is, net taxable income after adding back interest expense, taxes, depreciation, and amortization. The CARES Act makes the deduction limitation less restrictive for 2019 and 2020 in three ways.

Snaitech generated $285 million of adjusted EBITDA in 2023 and NSX is expected to report $34 million of adjusted EBITDA for 2024, according to New York-based investment bank Needham & Company. In 2020, the company completed a $12 billion acquisition of Canadian online gaming giant The Stars Group.

Uber’s financial horizon brightens with EBITDA breakeven, anticipating margins of 15-20%. In contrast, Lyft, on its path to profitability, eyes positive EBITDA margins in the higher single digits soon. ride-sharing market, with its share increasing from 62% in early 2020 to 74% more recently.

Some experienced record years during the peak of the lockdowns in 2020 based on their successful pivot to a combination of outdoor dining and take-home business. The average reported expected revenue growth rate was nearly 14% per annum during 2021 and 2022 and the average expected long term EBITDA margin was around 14%.

Coming in the week after ARM, an AI chip designer, also filed to go public, but with an estimated pricing of $55-$60 billion, it is an indication of how much the ground has shifted under Instacart since the heady days of 2020, when Instacart was viewed by some Americans as the only thing that stood between them and starvation.

billion of annual revenue and $560 million of EBITDA. The $2 billion Allegiant Stadium opened in 2020 as the home of the NFL’s Raiders franchise and will host Super Bowl LVIII in February 2024. Formula One Group, founded in 1950, was purchased for $4.4 billion in 2016 by Liberty Media. The subsidiary reports $2.8

Though far from their 2020 highs, revenue multiples have crept back up to a level that is more in line with long-term historical trends, which we generally consider to be healthy. Only 27 of the 62 companies with negative EBITDA margin also had negative cash flow. Last quarter, the median multiple hit 6.3X, also up from 5.6X

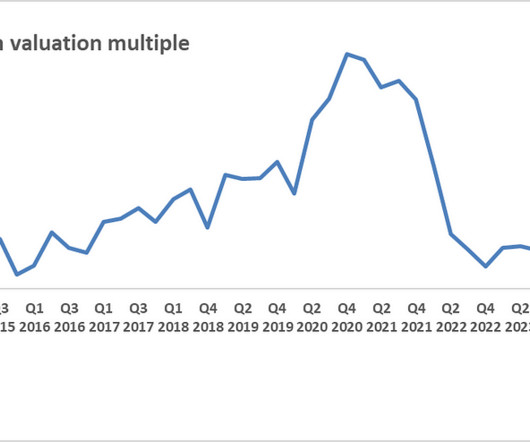

Feb 2023 data ] Industry EBITDA multiples, sourced from analysis by Prof. in February 2020, to 24.89 Two specific parameters are always worth a closer look, to understand how the market is developing: Average and Maximum startup valuation for the Scorecard and Checklist methods, derived from our analysis of Crunchbase deal data. [

billion acquisition of Slack in 2020. At the current level Salesforce has a P/E ratio of 100x and an EV/EBITDA ratio of 47x for 2022. This was mainly driven by operating expenses growth exceeding sales growth and thus putting strain on EBITDA margin. He played a major role in the $27.1 Salesforce announced total revenue of $7.8

billion acquisition of Slack in 2020. At the current level Salesforce has a P/E ratio of 100x and an EV/EBITDA ratio of 47x for 2022. This was mainly driven by operating expenses growth exceeding sales growth and thus putting strain on EBITDA margin. He played a major role in the $27.1 Salesforce announced total revenue of $7.8

The enterprise value of publicly traded alternative energy companies has risen from close to zero two decades ago to more than $700 billion in 2020, before losing steam in the last three years: Adding in the value of private companies and start-ups in this space would undoubtedly push up the number further. in the 2011-2023 time period.

2022 saw a robust cash and capital structure with a staggering USD 967 million adjusted EBITDA in Q4, up by 14% from the previous year. ’s share price witnessed growth leading up to 2020, bolstered by its solid financial performance and stable business model. Share Price Performance Oneok Inc.’s billion using a WACC of 10%.

If you Google this topic and look at the results, you’ll find articles and discussions about LBO models and points like the returns attribution analysis : This type of “value creation” measures the returns sources in a buyout deal: Debt paydown vs. multiple expansion vs. EBITDA growth.

2 | Industry EBITDA multiples used in the VC and DCF with multiple. As a result, the next question we need to examine is: Why did 2020 bring us the worst economic collapse since the Great Depression, yet the fastest venture market rebound ever? Our multiples are based on public market conditions at the beginning of current year.

billion in 2020. billion, driven by lower interest expense and lower non-cash impairment losses, offset by lower Adjusted EBITDA, an accrual related to the securities class action lawsuit, and higher supply chain and commodity costs. Adjusted EBITDA decreased 5.8% Net income increased 131.3% billion using a WACC of 6.3%.

billion in 2020. billion, driven by lower interest expense and lower non-cash impairment losses, offset by lower Adjusted EBITDA, an accrual related to the securities class action lawsuit, and higher supply chain and commodity costs. Adjusted EBITDA decreased 5.8% Net income increased 131.3% billion using a WACC of 6.3%.

With steady demand for footwear, many manufacturers brought production back in-house with global shutdowns during 2020. This includes SDE, REV, and EBITDA multiples for shoe & footwear manufacturing. EBITDA Multiples for Shoe & Footwear Manufacturing. Average EBITDA Multiple range: 4.08x – 4.76x.

EBITDA multiple or a cap rate of approximately 5.3% The Resort recently benefitted from a transformative renovation and was closed from March of 2020 to June of 2021. The acquisition price represents a 16.3x on the Resort's 2024 estimated results 1.

19-20298, 2020 WL 4814094 (5th Cir. 19, 2020), the United States Court of Appeals for the Fifth Circuit affirmed the dismissal of a putative class action suit under Section 14(a) of the Securities Exchange Act of 1934 (“Exchange Act”), 15 U.S.C. § In Heinze v. Tesco Corp. ,

With a revenue of C$ 943 million for financial year 2020-2021, BALL is dedicated to the processing and marketing of canned and frozen vegetables in the United States and Canada, in the retail supermarket and food service sectors, mainly with private labels, third party brands and own brands such as Arctic Gardens and Del Monte.

With a revenue of C$ 943 million for financial year 2020-2021, BALL is dedicated to the processing and marketing of canned and frozen vegetables in the United States and Canada, in the retail supermarket and food service sectors, mainly with private labels, third party brands and own brands such as Arctic Gardens and Del Monte.

Even assuming a top line growth rate superior to that of Match.com for the next 5 years, averaging over 20% (compared to 35% in 2019 and 19% in 2020, admittedly in adverse conditions due to the Covid lockdowns) the DCF for Bumble doesn’t make the case for much optimism. Our findings suggest a valuation of $4.6Bn may be more adequate.

What’s happening with the company Netflix has just experienced its largest rise of new subscribers since the COVID-19 lockdowns in 2020. Stock Market Implications In the recent past, most notably in 2020 and 2021, Netflix experienced considerable growth in the stock market. Last quarter, Netflix managed to add 8.8 Youtube), Apple Inc.

After reaching new highs in early 2020 of €420 per share, the share price fell due to economic conditions and Covid-19. Since trading at €320 in mid 2020, the share price has more than doubled to its current level of €780 per share. In early 2018 the company traded at €250 per share.

billion, showing a continuation of the robust performance achieved during the challenging economic conditions of 2020 when it grew profit before tax by 8%. . In the fo rmer, we compared Porsche with peers such as BMW, Mercedes-Benz, Ferrari and Ford using thethe EV/EBITDA and the EV/EBIT multiples. Porsche’s Future Goals.

The company already paid over CHF 100 million in settlement in this matter in 2020. . ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. IPO of E-Mobility Division. The intention is still to take the E-Mobility division public in the short term. Share Price Performance.

The company already paid over CHF 100 million in settlement in this matter in 2020. . ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. IPO of E-Mobility Division. The intention is still to take the E-Mobility division public in the short term. Share Price Performance.

times the combined acquired trailing twelve-month EBITDA. 487MM of cumulative inorganic capital investment in the profitable, high-growth Contractor Solutions segment since December 2020. Capital investment multiple of 6.6 Expected to be accretive to earnings per share in the first full year of ownership. DALLAS, Oct.

What’s changing 1 | Average valuations used in the Scorecard Method and maximum valuations used in the Checklist Method We base our estimates on real transactions by country since February 1st, 2020. You can refer to the table at this link to see how they will change for your country specifically.

million, potential EBITDA could be up to approximately $7.68 The Consideration Shares were issued to AI Renewable GP 2020 Ltd. (" AI GP 2020 "), resulting in AI GP 2020 becoming an insider of the Company by virtue of owning 11.9% million and potential net income up to approximately $1.64 Early Warning Disclosure.

million, potential EBITDA could be up to approximately $7.68 The Consideration Shares were issued to AI Renewable GP 2020 Ltd. (" AI GP 2020 "), resulting in AI GP 2020 becoming an insider of the Company by virtue of owning 11.9% million and potential net income up to approximately $1.64 Early Warning Disclosure.

Dust Free's trailing twelve-months' EBITDA, excluding future earn-outs, which if achieved would be incrementally accretive to CSWI Closed on two smaller acquisitions, totaling $2.9 Investment Highlights Capital investment of $27.4 06, 2024 (GLOBE NEWSWIRE) -- CSW Industrials, Inc. Investment Highlights Capital investment of $27.4

This is likely a result of increased demand during the 2020 pandemic. Below, we discuss SDE, EBITDA, and REV multiples for a medical supply company. EBITDA Multiples for a Medical Supply Company EBITDA multiples reflect a medical supply company’s earnings before interest, taxes, depreciation, and amortization.

After a breathtaking performance for one and a half years starting in 2020, the company suffered a dismal few months. billion by applying the observed multiple EV/EBITDA for 2024 and EV/Sales. However, once profitability is achieved, management intends to push growth on this platform again. Share Price Performance. billion to $41.6

For example, if a three-year time-vesting grant of 300,000 shares is made to a CEO on Jun 30, 2020, the CEO typically will have full ownership of 100,000 shares on June 30, 2021; another 100,000 shares on June 30, 2022; and the remaining 100,000 shares on June 30, 2023. firm-years (i.e., We find that only 6.4

billion and ~$150 million in pro forma cash on the combined company balance sheet with a combined ~12% EBITDA margin 1 , and no debt or equity financing contemplated. Industry Leading Financial Profile : Estimated LTM combined revenue of $1.2 Turnaround of a 28-year-old Metals Technology : Full story available on Benzinga.com

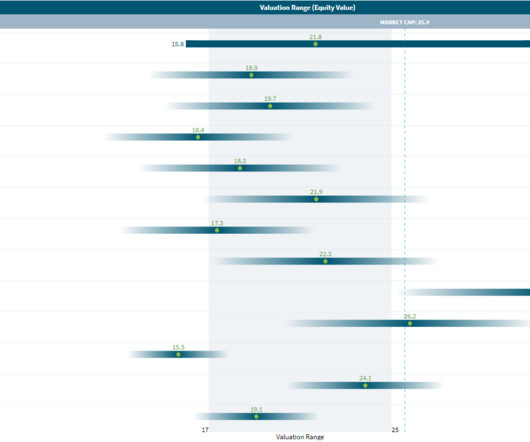

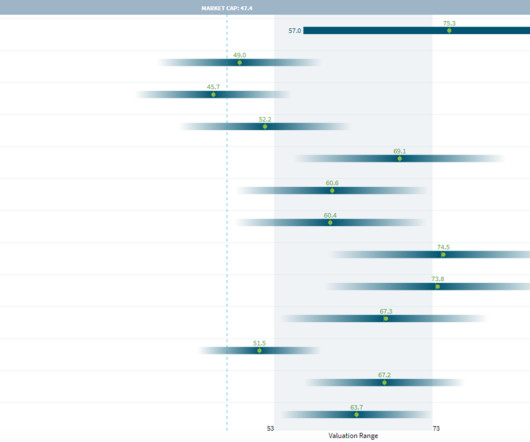

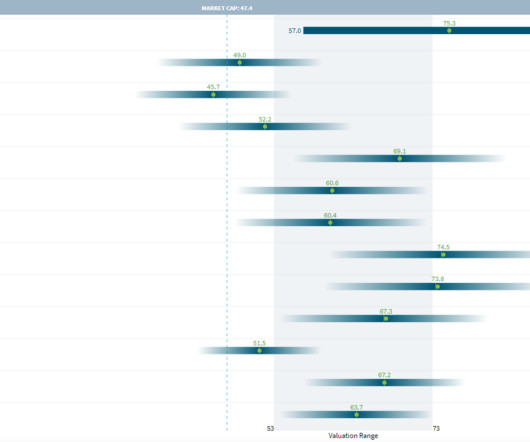

Despite a -21% performance in 2022 to date, Home Depot’s share price gained 64% over the past five years, with particularly good performance during the 2020-2021 COVID years. The Trading Comparables analysis resulted in a valuation range of $202 billion to $231 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E.

Despite a -21% performance in 2022 to date, Home Depot’s share price gained 64% over the past five years, with particularly good performance during the 2020-2021 COVID years. The Trading Comparables analysis resulted in a valuation range of $202 billion to $231 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content