This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on marketcapitalization and price to book ratios.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Return on (invested) capital 2.

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments.

The first is the dividends you receive, while you hold stocks, a cash flow stream that provides a measure of stability to investors who seek it. trillion in marketcapitalization, but for balance, it is also worth noting that US equities are still holding on to a gain of $6.9

My two most recent valuations were in June 2019 and January 2020, and I am going to go back to them, not just because they are recent, but because they led to investment decisions on my part. In June 2019, Tesla had hit a rough spot, partly due to concerns about production bottlenecks and debt, and partly due to self inflicted wounds.

Investors, used to a decade of better-than-expected earnings and rising stock prices at these companies, have been blindsided by unexpected bad news in earnings reports, and have knocked down the marketcapitalization of these companies by hundreds of billions of dollars in the last few weeks.

Furthermore, the company increased dividends by 10% and announced that it will buy back GBP 2.3 (USD In 2019, the company announced that it plans to reduce its oil and gas output by 40% by 2030. In comparison to BP’s marketcapitalization of GBP 101 (USD 122) billion we suggest that the company is slightly undervalued.

This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%. This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years.

This strong financial performance is also reflected in the stock market as TotalEnergies is currently trading at €57 per share, which is a year-on-year increase of roughly 30%. This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years.

In this post, I want to focus on that point, starting with a discussion of why stories matter to investors and traders and the story that propelled the company to a trillion-dollar marketcapitalization not that long ago. billion in revenues in 2021.

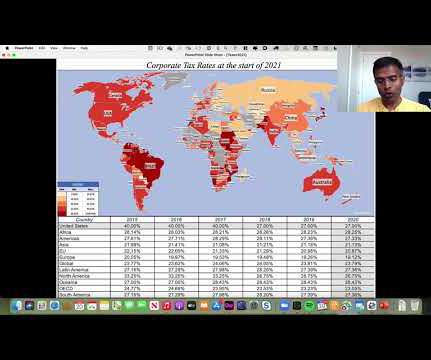

While the universe of companies is diverse, with approximately half of all firms from emerging markets, it is more concentrated in marketcapitalization, with the US accounting for 40% of global marketcapitalization at the start of the year.

This was primarily based on revenue growth, which registered a heady 30% rise, allowing the bank to distribute its highest full-year dividend since 2008. The group’s marketcapitalization in 2023 was at a 17-year high, valuing the enterprise at around the same level in dollar terms as Goldman Sachs. billion in 2022.

In 2021, companies recovered entirely from the damage done in 2021, at least in the aggregate, with earnings in 2021 higher than 2019 earnings, by almost 33%. The largest sector, in the US, in terms of marketcapitalization, is information technology and I have argued that tech companies age in "dog years" , with compressed life cycles.

When you augment this price change with the dividends on the index during 2021, the total return on the S&P 500 for 2021 was 28.47%. the 2019-21 time period would rank 8th on the list of 92 3-year time periods. that was earned in 2019 (pre-COVID).

In a predictable consequence, US multinationals chose to leave their foreign income outside the US, creating the phenomenon of trapped cash, i.e., income held in foreign locales to avoid taxes, but also trapped because that income could not be used to pay dividends, buy back stock or invest in projects in the United States.

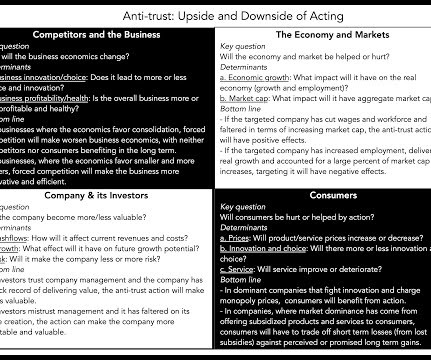

If, by allowing a company or companies to reach a dominant position in the market, you are increasing their competitive advantages against foreign competitors or adding to the aggregate payoff to investing in stocks in markets, should you put those gains at risk by handicapping those companies?

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content